Normally, when you start searching for a mortgage, one of your first choices is between a government-backed loan and a conventional loan. You will want to know about the conventional loan down payment percentage in real estate by using mortgage payment calculator.

Among borrowers, conventional mortgages are the most widely supported mortgage option. However, when it’s time to decide on the mortgage you’ll use for buying a home or refinancing, it’s crucial to grasp the kind of mortgage you’re eligible for and what aligns with your requirements.

Keep reading to get insights into conventional loans and determine if this type of mortgage is the right fit for you. Meanwhile, you can find out How Much is Mortgage Payments? It will help you to calculate Interest rate, Taxes and Insurance when using Online Calculator.

Here’s the key information in this guide broken down for you:

- No Government Backing, Stricter Rules: Unlike government-backed options, a conventional mortgage lacks government support and comes with more stringent qualification criteria.

- Conforming and Nonconforming: Conventional mortgages can be categorized as either conforming or nonconforming. The majority of borrowers opt for conforming mortgages.

- Qualification Hinges on Credit and More: Eligibility for a conventional mortgage often depends on various factors, including a solid credit score, among other considerations.

What is a Conventional Mortgage loan?

A conventional mortgage, also known as a conventional loan, is a type of mortgage that isn’t protected or guaranteed by a government agency. In short, it is not a government-backed loan.

When you opt for a conventional mortgage, you’ll secure it through a private lender like a bank, non-bank mortgage lender, or credit union. Although these mortgages lack government insurance, a lot of them receive support from government-sponsored enterprises like Fannie Mae and Freddie Mac. This often means that the mortgage will be sold to one of these organizations after the closing process.

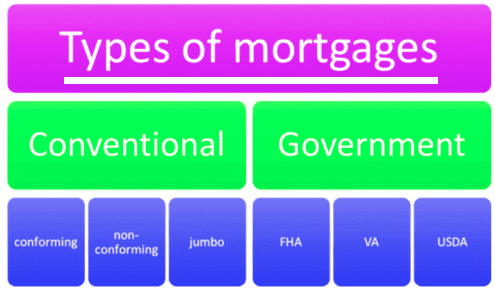

Conventional vs. Government-backed Mortgage

In a simple understanding, a government-backed mortgage includes a form of insurance or assurance from a federal agency like the Federal Housing Administration, United States Department of Agriculture, or Department of Veterans Affairs. This safeguard ensures that if the borrower is unable to make payments, a portion of the mortgage will be covered by the government.

Since conventional mortgages lack this insurance, they typically have more stringent eligibility criteria. To qualify for a conventional mortgage, you’ll generally need a higher credit score, a lower debt-to-income ratio, and a larger down payment.

Types of Conventional Mortgages

Conventional mortgages can be divided into two main groups: conforming and nonconforming loans. The main difference between these mortgage categories is the amount of money you intend to borrow.

A conforming mortgage aligns with the limits established by the Federal Housing Finance Agency (FHFA) and meets the criteria necessary for purchase by lenders like Fannie Mae or Freddie Mac. These conforming loan limits are adjusted annually by the FHFA. For 2023, the limit is $726,200 in most parts of the US, while in regions with higher living costs, it can go up to a maximum of $1,089,300.

On the other hand, a nonconforming mortgage doesn’t fulfill these criteria. One common form of nonconforming mortgage is known as a jumbo loan, which surpasses the established conforming loan limits.

Qualifying for a nonconforming mortgage, like a jumbo loan, might require a higher credit score, a larger down payment, and a lower debt-to-income ratio compared to what’s necessary for a conforming loan.

Who qualifies for a Conventional mortgage?

First of, you have to know the list of requirements and documents to apply for Mortgage [Home Loan] before you continue. In general, to qualify for a conventional mortgage you need to meet some eligibility requirements to qualify for mortgage. This can be divided into three main areas: your credit score, your debt-to-income ratio, debt level and the down payment you can make.

If you find it challenging to meet all three of these criteria, it’s a good idea to explore whether you’re eligible for a government-backed mortgage or consider delaying your home purchase. With additional time, you can work on enhancing your credit score, reducing your debts, or increasing your savings for a down payment. This could improve your chances of qualifying for a conventional mortgage in the future.

1. Credit Score required for Conventional Loan

To be eligible for a conforming conventional loan, you generally need a credit score of at least 620, although certain lenders might ask for even higher scores. However, if you’re considering a nonconforming loan, such as a jumbo loan, it’s likely that you’ll need a credit score of 700 or higher. There’s a guide to check your credit score.

2. Debt-to-income ratio for Conventional Loan

Your debt-to-income ratio (DTI) is determined by dividing your monthly debt payments by your total monthly income. For example, if you spend $2,000 every month on mortgage and student loan payments, and you earn $3,000 per month, your DTI ratio is calculated as $2,000 divided by $3,000, which equals 66%.

When you’re applying for a mortgage, the potential future mortgage payment is considered in this calculation. For conforming conventional mortgages, you might be eligible with a total DTI ratio of up to 50%. However, the highest DTI you can have depends on your overall financial situation, including your credit score and the down payment you can make. To improve your chances of approval, it’s recommended to keep your DTI under 36%.

If you’re pursuing a jumbo loan, having a DTI ratio above 45% might make it more challenging for you to qualify. See how to Calculate your debt-to-income ratio.

3. Down payment for Conventional Loan

When it comes to conforming loans, you can make a minimum down payment of 3%, but certain lenders might ask for 5% or 10%. As for jumbo loans, the required down payment can be 10% or higher, varying between different lenders.

If you decide to put down less than 20% on a conforming loan, you’ll be required to pay for private mortgage insurance (PMI) until your equity in the home reaches 20%. This monthly expense will be combined with your mortgage payments. Typically, you’ll pay around $30 to $70 each month for every $100,000 you borrow, as indicated by Freddie Mac.

Helpful Conventional Loan Mortgage Insights

- Best Strategies to Improve Your Credit Score from 500 to 800

- Credit Score Check, Reports and Highest Range in Your Finance

- How to Remove Repossession Report Out of Your Credit Report

- Repo: How Long Does a Repossession Affect Your Credit Score?

- Repossession Law and its Consequences on Your Credit Report

- Can I Get a Home or Car Loan with a Repossession on my Credit?

- Home Equity Lines of Credit (HELOCs) What it is and How to Access it

- What is Credit Facility? How it Works for Personal & Business Loan and Mortgage

Conventional Mortgage Interest Rates

Conventional mortgage rates typically tend to be slightly higher compared to rates for government-backed loans. However, certain government-backed loans may have additional fees that could potentially make them more expensive than the slightly higher conventional rate.

When you’re weighing the choice between a conventional or government-backed mortgage, it’s important to perform the necessary calculations rather than assuming that a lower rate is automatically the better choice.

Below are the elements that influence your conventional loan interest rate:

- Economy

- Where you live

- Personal finances

- Loan Term

- Term length

- Mortgage Points

Now, lets explain them in details for easier understanding for layman.

1. Economy

The economic conditions significantly influence mortgage rates. In times of slow economy, rates usually decrease due to reduced demand from borrowers.

In the years 2020 and 2021 for example, mortgage rates reached went down due to some responses from policy moves. This drop was a result of actions taken by the Federal Reserve to stabilize the economy during the pandemic.

Looking at it from another angle, during periods of economic growth, mortgage rates tend to rise due to increased demand from borrowers. Additionally, elevated inflation resulting from a robust economy can also push mortgage rates higher. This phenomenon has been observed over the past eighteen months.

2. Where you Live

Over the years, you might have observed that homes in cities often come with higher price tags compared to rural areas. Moreover, certain cities and states can have varying housing costs.

Yet, it’s important to note that your geographical location also influences your interest rate. Typically, areas with a higher cost of living tend to have slightly higher interest rates, although the difference shouldn’t be significantly large.

3. Personal Finances

It’s important to understand that your credit score, debt-to-income ratio, and down payment not only play a role in whether you’ll be approved for a conventional mortgage, but they also influence your interest rate.

This means that, the stronger your financial standing, the lower your interest rate is likely to be. Borrowers can secure a more favorable rate by having a credit score of 670 or higher, maintaining a debt-to-income ratio under 36%, or making a down payment of at least 20%. These factors collectively contribute to obtaining a better interest rate on your mortgage.

4. Loan Term

When deciding on a mortgage, you’ll have to choose between two options: a fixed-rate mortgage or an adjustable-rate mortgage (ARM).

A fixed-rate mortgage secures a consistent interest rate for the entire duration of your loan. Despite fluctuations in US mortgage rates over time, your interest rate remains unchanged throughout the 30-year term. This means your rate will stay the same from your first payment to your last.

Conversely, an adjustable-rate mortgage (ARM) maintains a steady rate for the initial years, and then adjusts periodically, often once or twice annually.

Choosing an ARM might make sense if you’re not purchasing a long-term residence, as you could potentially move before facing a rate increase. This makes it a viable choice for those who anticipate relocating before any potential rate adjustments.

5. Term length

Another choice you’ll make is selecting a term length, which determines the number of years it will take to fully repay your loan.

For fixed-rate mortgages, the 30-year term is the most prevalent choice. Lenders often offer 15-year and 20-year options as well, and some provide even more alternatives.

In the case of an adjustable-rate mortgage, the 5/1 ARM is the most typical. Your rate remains unchanged for the initial five years, after which it adjusts annually. Many lenders also present 7/1 and 10/1 ARMs.

It’s important to note that the longer your chosen term, the higher your interest rate may be.

6. Mortgage Points

What are mortgage points and how do they work? Closing Cost on Mortgage are the expenses you need to pay when you get a loan, whether you are buying a property or refinancing.

During the closing cost process, you have the option to pay a fee known as mortgage points. The benefit of this is that the more points you pay, the lower your interest rate becomes.

However, it’s worth noting that FHA loans frequently come with lower interest rates than conventional loans, making them a potentially more affordable option for those who have less stable credit histories.

Typically, one mortgage point equals 1% of your total mortgage amount. For instance, if your loan is $100,000, one point would cost you $1,000.

On average, one point tends to lower your interest rate by around 0.25%.

For illustration, suppose you’re purchasing a home with a $100,000 mortgage at a 3.5% interest rate. If you choose to pay $2,000 in closing for two mortgage points, your rate will drop by a total of 0.5%. Consequently, you’ll only be paying 3% on your loan after this adjustment.

Conventional mortgage Frequently Asked Questions

Is conventional better than FHA?

Conventional loans might offer advantages over FHA loans if you possess a robust financial standing. Individuals with good credit scores, minimal debt-to-income ratios (DTIs), and substantial down payments typically find that conventional loans are more cost-effective compared to FHA loans.

Do you have to put 20% down on a conventional loan?

Absolutely yes, you are not obligated to make a 20% down payment on a conventional loan. This is a common misconception. While 20% is the threshold to avoid Private Mortgage Insurance (PMI), many borrowers opt for lower down payments. In fact, you have the flexibility to put down as little as 3% on a conventional loan.

Is it difficult to get approved for a conventional loan?

While conventional loans come with stricter criteria compared to government-backed mortgages, it’s important to note that obtaining approval for a conventional loan isn’t significantly more challenging for most borrowers. Your likelihood of approval increases with better credit and stronger financial standing.

What is the lowest down payment for a conventional loan?

You have the option to make a minimum down payment of 3% on a conventional loan, and it’s worth noting that some lenders may have slightly higher requirements, such as 5% or 10%. This allows for a range of options based on your financial situation.

Why would someone only accept a conventional loan?

In some instances, homebuyers using FHA loans might encounter challenges in having their offers accepted compared to those with conventional financing. Home sellers often prioritize offers that promise a smooth and timely closing process with minimal complications.

Consequently, offers backed by conventional loans may be more appealing to sellers due to the faster closing timelines and fewer appraisal and repair stipulations. FHA loans, in contrast, can sometimes involve additional steps that could potentially slow down the transaction.

Conclusion

In conclusion, choosing between a conventional loan or mortgage requires careful consideration of your financial circumstances and goals. Conventional loans, while having more stringent requirements, can offer some mortgage advantages.

They include lower interest rates for borrowers with strong credit and larger down payments. They provide options in terms of down payment, ranging from 3% to potentially higher percentages.

On the other hand, government-backed loans like FHA may be more suitable for those with lower credit scores or smaller down payments, offering competitive rates and easier eligibility.

The decision ultimately depends on factors such as your credit score, debt-to-income ratio, down payment capability, and the specific terms that align with your homebuying aspirations.

Lastly, make sure your thoroughly evaluate your financial situation and comparing the benefits and limitations of both options. With that, you can make a better choice that best suits your needs and paves the way for a successful home purchase journey.

Helpful Guides

- Refinancing Your Home: The Pro’s and Con’s of Mortgage Refinancing

- Balloon Payment Mortgage: What it is, How it Works, and it Pros and Cons

- First Time Mortgage Buyer: Preparation and Tips on Home Purchasing

- Home Loan: How to Apply Mortgage, it’s Benefits and Documents Required

- How to Find the Best Loan options when Shopping for a Home Mortgage Loan?

- FHA Loan is Government-backed Mortgage insured by the Federal Housing Administration

- Key Documents Needed to Apply for Home Loan in Nigeria [Mortgage Application Guide]

![How Much is Mortgage Payments?Calculate using Interest rate, Taxes and Insurance [Online Calculator]](https://hybridcloudtech.com/wp-content/uploads/2023/06/How-Much-is-Mortgage-PaymentsCalculate-using-Interest-rate-Taxes-and-Insurance-Online-Calculator-100x70.png "How Much is Mortgage Payments? Calculate using Interest rate, Taxes and Insurance [Online Calculator]")

Requirements, How to Calculate LTV in Mortgage")