Financial security in retirement doesn’t just happen if you don’t prepare for it. It takes early planning, goals execution and commitment and, yes, money in the key.

In this article, we will review the top 10 ways to prepare for your retirement from an early stage. Everything you need to know about planning, government policies, saving guidelines etc is provided in this post.

Facts that people don’t prepare for Retirement in the US

1. Lack of Financial Literacy:

One of the biggest reasons why people don’t prepare for retirement in the US is because of a lack of financial literacy. Many individuals don’t have a clear understanding of how much money they need to save for the future, how to invest their money, and how to manage their finances effectively. Without this knowledge, it’s easy to underestimate the amount of money needed to retire comfortably and fail to take action to save for days to come.

2. High Living Expenses:

Another reason why many people don’t prepare for retirement in the US is because of high living expenses. In many cases, individuals are struggling to make ends meet on a day-to-day basis and simply don’t have the resources to save for retirement. This is particularly true for those who live in expensive cities or have high levels of debt.

3. Dependence on Social Security:

Many people in the US rely on Social Security as their primary source of retirement income, which is not enough to provide for a comfortable future. However, despite this, many people still fail to save for retirement because they believe that Social Security will be enough to cover their expenses. This can lead to financial hardship in retirement, as Social Security benefits are often not enough to cover all of the expenses associated after you retire.

Key Note

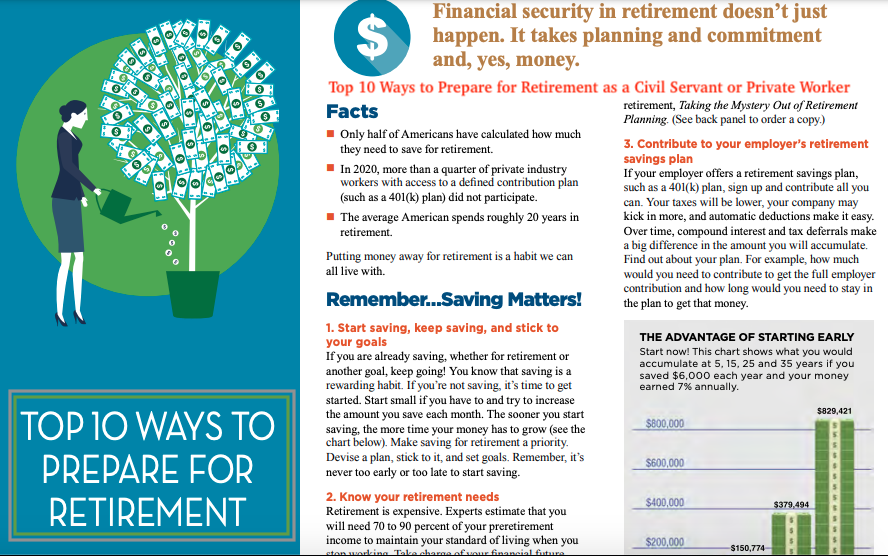

From experience, only about half of American population have calculated how much they need to save for retirement benefit. Last year, more than a one third of private industry workers did not participate in contribution plan (such as a 401(k) plan). Most of then even had access to a defined contribution. In reality, an average American citizen spends about 20-25 years in retirement before they pass on. With that in mind, saving money for retirement benefit is a habit we can all must live with if we must be happy.

You mayAlso Like this

- House Mortgage – Meaning, Types, Loans and How it Works

- What is Mortgage Home Loan, Types and Process of Securing it?

- The Role of The Attorney General in Taxation and Tax-Related Matters

- Perfection of Legal Mortgage in Nigeria Law & Procedure for Loan Property

- How Much is Mortgage Payments? Calculate using Interest rate, Taxes and Insurance [Online Calculator]

Does Saving for Retirement Matter? Yes, it does!

1. Start saving, keep saving, and stick to your goals

“Start saving, keep saving, and stick to your goals” is a wise and effective piece of advice for anyone who wants to prepare for retirement or achieve any financial goal. My advice; if you are already saving for retirement, continue! We all know that saving is a rewarding habit for everyone.

On the other hand, if you’re currently not saving any money, now is the best time to begin. Start saving small if you have to, then try harder to increase the amount you save every month and the money will grow. Make saving for old age after you retire a priority.

See the importance of the saving process:

- Start Saving: The first step in achieving any financial goal is to start saving money. This means setting aside a portion of your income every month or every pay-check and putting it into a savings account or retirement fund. The earlier you start saving, the more time your money has to grow, thanks to compound interest.

- Keep Saving: Once you’ve started saving, it’s important to continue doing so consistently. This means making saving a priority and sticking to your savings plan even when other expenses or temptations arise. You may need to adjust your budget or cut back on certain expenses to make sure you’re saving enough to meet your goals.

- Stick to Your Goals: Finally, it’s important to stay focused on your goals and not get sidetracked by short-term distractions or setbacks. This means having a clear idea of what you’re saving for and why it’s important to you. It also means being patient and persistent, even when progress seems slow or difficult.

By following these principles, you can build a solid foundation for your financial future or achieve your long-term goals. It can be a comfortable retirement, a down payment on a house, or something else entirely.

2. You Must Know your Retirement Needs

Knowing your retirement needs involves estimating how much money you’ll need to live on after you retire.

Here are some steps you can take to determine your retirement needs:

- Determine your retirement age: Decide at what age you plan to retire. This will give you an idea of how many years you’ll need to save for.

- Estimate your retirement expenses: Consider what your expenses will be during retirement. Think about the cost of housing, transportation, food, healthcare, travel, and any other expenses you expect to have.

- Calculate your retirement income: Determine how much money you’ll receive from Social Security, pensions, annuities, and other sources of retirement income.

- Determine your retirement savings gap: Calculate the difference between your estimated expenses and your retirement income. This will give you an idea of how much money you need to save before you retire.

- Adjust for inflation: Consider how inflation may impact your expenses during retirement. You may need to adjust your estimated expenses upward to account for inflation.

- Consult with a financial advisor: A financial advisor can help you estimate your retirement needs and develop a plan to achieve your retirement goals.

By following these steps, you can get a better understanding of how much money you’ll need to save for retirement and what steps you need to take to achieve your retirement goals.

3. Always Contribute to your employer’s retirement savings plan

Contributing to your employer’s retirement savings plan is a smart financial move that can help you save for retirement while also taking advantage of any employer matching contributions.

If a retirement savings plan, such as a 401(k) plan, is offered by your employer, it is recommended that you signup for it too so as to increase your contributions. By contributing to your plan, you can lower your taxes, receive potential company contributions, and benefit from the convenience of automatic deductions.

Through the power of compound interest and tax deferrals, the amount you accumulate can significantly increase over time. It’s important to understand the details of your plan, such as the minimum contribution required to receive the full employer contribution and the duration of participation needed to obtain that money.

Here are some steps to follow:

- Review the plan: First, review the details of your employer’s retirement savings plan, including the contribution limits, investment options, and any employer matching contributions.

- Decide on a contribution amount: Determine how much you can comfortably afford to contribute to the plan each paycheck. Try to contribute enough to take full advantage of any employer matching contributions, if available.

- Set up automatic contributions: Most retirement plans allow you to set up automatic contributions from your paycheck, which can make it easier to save consistently over time.

- Monitor your investments: Check in on your investment choices periodically to make sure they align with your retirement goals and risk tolerance. Additionally, you may want to adjust your investments over time as your goals or financial situation changes.

- Consider a financial advisor: If you’re not sure where to start with your retirement planning, consider seeking the advice of a financial advisor who can help you set goals and make a plan to reach them.

Lastly, you have to remember this; saving for retirement is an important part of financial planning. Also, contributing to your employer’s retirement savings plan can help you reach your goals more quickly.

4. Ask around to Learn about your Employer’s Pension plan

If your employer offers a conventional pension scheme, make sure to confirm your enrollment in the plan and comprehend its mechanics. Request a personal statement of benefits to evaluate the value of your benefit.

Before switching jobs, determine the potential impact on your pension benefit. Make sure you familiarize yourself with any benefits you may have accrued from previous employment and inquire about eligibility for benefits from your spouse’s plan.

How to Learn about your Employer’s Pension Plan

To learn about your employer’s pension plan, you can follow these steps:

- Speak with your HR representative: Contact your employer’s human resources (HR) department or your supervisor to ask for information about your pension plan. They can provide you with the plan documents and answer any questions you may have.

- Review the pension plan documents: Carefully review the plan documents that HR provides you with, including the plan’s summary plan description, which explains the plan’s benefits, eligibility requirements, vesting schedules, and other important information.

- Understand the plan’s features: Learn about the various features of the pension plan, such as the type of plan (defined benefit or defined contribution), the investment options available, and the contribution and matching policies.

- Know your options: Understand the options available to you, such as how to enroll in the plan, how to change your contribution level, and how to select investment options.

- Seek professional advice: If you have any questions or concerns about your pension plan, seek professional advice from a financial advisor or a retirement planning specialist.

Remember, it is important to take an active role in your retirement planning, and understanding your employer’s pension plan is an important part of that process.

5. Take into account Fundamental Principles of Investing

Financial security is not solely determined by the amount you save, but also by how you save. The impact of inflation and the type of investments you choose cannot be overstated, as they greatly affect your retirement savings. To ensure your financial well-being, it is essential to understand how your savings or pension plan is invested.

Try and familiarize yourself with the investment options available to you and ask questions when necessary. Diversifying your savings across different types of investments can help to mitigate risk and increase returns. However, keep in mind that your investment mix may change over time based on factors such as your age, goals, and financial circumstances. Ultimately, financial security and knowledge are interdependent.

Basic Investment Principles to Consider for Retirement

Retirement investment involves planning for the long term and ensuring that you have enough money to support yourself during your retirement years. Here are three basic principles of retirement investment:

- Start early: One of the most important principles of retirement investment is to start saving and investing as early as possible. The earlier you start, the more time your investments have to grow and compound, potentially resulting in a larger retirement nest egg. Even small contributions made over a long period of time can add up significantly.

- Diversify your portfolio: As with any investment strategy, diversification is crucial for retirement investing. By investing in a mix of assets, such as stocks, bonds, and real estate, you can potentially reduce your risk and improve your chances of earning higher returns over the long term. Diversification helps ensure that you don’t have all your eggs in one basket, which can be especially important as you near retirement age.

- Plan for inflation: Inflation is a real risk for retirees, as the cost of living tends to rise over time. To ensure that your retirement savings keep pace with inflation, it’s important to invest in assets that offer some protection against inflation, such as stocks, real estate, and inflation-indexed bonds. It’s also a good idea to periodically review your retirement plan and adjust your savings and investment strategy as needed to account for changing economic conditions and your own changing financial goals.

Bottom Line

Try Diversification by spreading your money across different types of investments, such as stocks, bonds, real estate, and commodities, among others. Be cautious of time since investing is a long-term game, and it’s important to have a clear understanding of your investment time horizon. Lastly, be careful with risk tolerance since it iso the level of risk you are comfortable taking on in your investments. It’s important to understand your risk tolerance before investing, as it can help you determine the types of investments that are most suitable for you.

6. Don’t touch your retirement savings

It’s not advisable to touch your retirement savings. Withdrawing your retirement funds at this time could result in losing both the principal and the interest accrued. Additionally, you might forfeit certain tax benefits or even face withdrawal penalties. In the event that you change jobs, it’s recommended that you keep your savings invested in your current retirement plan, or alternatively, roll them over to an IRA or your new employer’s plan.

How do I manage so that I won’t touch my retirement money?

Managing your retirement savings can be challenging, but there are steps you can take to help ensure you don’t touch your retirement money prematurely. Here are some suggestions:

- Create a budget: One of the best ways to avoid dipping into your retirement savings is to create a budget and stick to it. Figure out your monthly expenses and set aside enough money from your income to cover them. This will help you avoid overspending and dipping into your retirement savings.

- Build an emergency fund: To avoid dipping into your retirement savings in case of an emergency, create an emergency fund. Start by setting aside a small portion of your income each month and gradually build it up over time.

- Automate savings: Set up automatic contributions to your retirement account so that a portion of your income is automatically directed towards your retirement savings. This way, you won’t have to rely on willpower to save, and the money will be out of sight and out of mind.

- Educate yourself: Learn about the different investment options available to you and the risks and benefits associated with each. This will help you make informed decisions about your retirement savings.

- Consider seeking professional advice: Consult with a financial advisor to help you create a retirement plan that aligns with your financial goals and risk tolerance. A financial advisor can also provide guidance on how to avoid dipping into your retirement savings prematurely.

Remember, your retirement savings are for your future, so it’s important to manage them carefully. By following these tips, you can help ensure that you don’t touch your retirement money until you’re ready to retire.

7. Request a Retirement Startup Plan from you Employer

Go and ask your employer to start a retirement plan. If your employer does not currently provide a retirement plan, you could propose the idea of establishing one. There are various saving plan alternatives accessible, and your employer could potentially establish a simplified plan that benefits both parties.

How to ask employer for your Retirement plan

Asking your employer about their retirement plan is an important step towards planning for your own retirement. Here are some tips on how to ask your employer about their retirement plan:

- Schedule a meeting with your employer: Request a meeting with your employer or human resources representative to discuss their retirement plan.

- Be clear and specific: When you meet with your employer, be clear and specific about what you want to know. Ask about the types of retirement plans that are available, such as 401(k)s, pension plans, or other options.

- Ask about eligibility: Find out if you are eligible to participate in the plan and if there are any requirements you need to meet.

- Inquire about contributions: Ask about the employer’s contributions, if any, and if there is a matching program for employee contributions.

- Clarify vesting: Understand how long it will take for you to become vested in the plan and what happens if you leave the company before becoming fully vested.

- Discuss investment options: Find out what investment options are available within the plan and what fees may be associated with those options.

- Seek clarification: Don’t be afraid to ask for clarification if you don’t understand something. It’s important to fully understand the retirement plan in order to make informed decisions about your future.

Remember, asking your employer about their retirement plan is an important step in planning for your own retirement. Don’t hesitate to ask questions and seek out information to make the best decisions for your future.

8. Start Putting money into an Individual Retirement Account

An Individual Retirement Account (IRA) allows you to contribute up to $6,000 annually. If you’re 50yrs of age or above, you can contribute even more. There is also an option to start with a smaller amount. Additionally, IRAs offer tax benefits.

There are two types of IRAs – traditional and Roth – and the tax treatment of your contributions and withdrawals will vary depending on which one you choose. The after-tax value of your withdrawal will also be affected by inflation and the type of IRA you select. See more information on IRA plan.

IRAs are a convenient way to save money, as you can set up automatic deductions from your checking or savings account and transfer them directly to your IRA.

Steps to put money into my Individual Retirement Account

- Determine the type of IRA you have: There are two types of IRA, Traditional IRA and Roth IRA. Each has different rules for contributions and withdrawals. You should know which type of IRA you have before making contributions.

- Decide how much to contribute: The IRS sets contribution limits for both Traditional and Roth IRAs each year. For 2023, the contribution limit is $6,000 for those under 50 and $7,000 for those 50 and over. Make sure you do not exceed the annual contribution limit.

- Choose a financial institution: You will need to open an IRA account with a financial institution such as a bank, brokerage firm, or mutual fund company. Choose one that offers low fees and a wide range of investment options.

- Open an IRA account: Follow the instructions provided by the financial institution to open an IRA account. You will need to provide personal information and designate the type of IRA you want to open.

- Fund your IRA: Once your account is open, you can fund your IRA in one of two ways – either with a lump sum or through regular contributions. If you choose to make regular contributions, set up automatic deposits to ensure you contribute consistently.

- Invest your contributions: Your IRA contributions will not grow unless you invest them. Choose the investments that match your investment goals and risk tolerance.

- Monitor your IRA: Regularly monitor the performance of your IRA investments to ensure they are meeting your goals. Consider making adjustments you notice a decline in your earnings or performance.

9. Find out about your Social Security Benefits

Typically, Social Security retirement benefits provide retirement beneficiaries with approximately 40 percent of their pre-retirement income. To get an idea of your estimated benefit amount, you can use the retirement estimator tool on the Social Security Administration website. For additional information, you can visit their website or contact them at 1-800-772-1213.

How do i know my Social Security Benefits?

To find out your estimated social security benefits, you can create an account on the Social Security Administration (SSA) website at www.ssa.gov. Once you have created an account, you can view your estimated benefits statement online.

Alternatively, you can call the SSA at 1-800-772-1213 and request your benefits statement over the phone. You can also visit your local Social Security office and ask for a benefits statement in person.

Your estimated benefits statement will include information about how much you can expect to receive in retirement benefits, disability benefits, and survivor benefits based on your earnings history and other factors.

10. Ask lots of Questions from Reliable Sources

Although these tips are intended to provide some guidance, they may not be sufficient. It is recommended that you read more of our publications listed on hybridcloudtech.com for more information. You should also consider seeking advice from your employer, bank, union, or a financial adviser. It is important to ask questions and ensure that you comprehend the responses. Take action and obtain practical advice as soon as possible.

For More Information to Help you Plan Your Retirement:

Visit the Employee Benefits Security Administration’s website to view the following publications:

- Savings Fitness: A Guide to Your Money and Your Financial Future

- Taking the Mystery Out Of Retirement Planning

- What You Should Know About Your Retirement Plan

- Filing a Claim for Your Retirement Benefits

- Women and Retirement Savings

- Retirement Toolkit

- Choosing a Retirement Solution for Your Small Business

To order copies, contact EBSA electronically or by calling toll free 1-866-444-3272. See more updates on Insurance for your health here.

The following websites can also be helpful resources:

- AARP

- American Savings Education Council

- Certified Financial Planner Board of Standards

- Consumer Federation of America

- The Actuarial Foundation

- U.S. Department of the Treasury

- U.S. Securities and Exchange Commission

Article Reference: Employee Benefits Security Administration United States Department of Labour.

Requirements, How to Calculate LTV in Mortgage")