Today, I will show you how to Calculate Debt-to-income Ratio for a Mortgage. It is the guide on understanding and calculating the debt-to-income ratio (DTI) for a mortgage. When you’re considering the exciting prospect of buying a new home, it’s important to have a clear grasp of your financial standing.

The debt-to-income ratio serves as a fundamental tool for both lenders and borrowers in the mortgage application process. It provides a comprehensive snapshot of your financial health by comparing your monthly debt payments to your gross monthly income.

In this guide, we’ll break down the significance of DTI, explain its components, and walk you through step-by-step instructions in mortgage on how to calculate it. By the end, you’ll have a deeper understanding of how lenders assess your eligibility for a mortgage based on your debt-to-income ratio, empowering you to make informed financial decisions on your journey to homeownership.

What is a debt-to-income ratio?

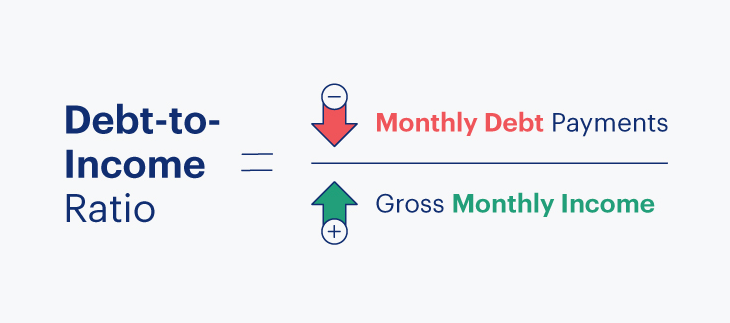

Your debt-to-income ratio (DTI) is all your monthly debt payments divided by your gross monthly income. This number is one way lenders measure your ability to manage the monthly payments to repay the money you plan to borrow. Source: Consumer Financial Protection Bureau (CFPB).

How to Calculate Debt-to-income Ratio for a Mortgage

1. Make a List of all your monthly debt payments

In finances, when we talk about monthly debts, we’re referring to the money you owe for things like car loans, student loans, mortgages, personal loans, child support, alimony, and credit cards.

However, it’s important to note that when we calculate your debt-to-income ratio, we focus on the smallest amount you need to pay for your credit cards, not what you usually pay.

It’s also good to remember that certain regular expenses like utility bills for your home, health insurance, life insurance as well as car insurance are not counted as debts in this calculation. This helps give a clearer picture of your financial situation.

2. Get Hold of your gross monthly income

Your gross monthly income is the total amount of money you earn before any taxes or deductions are taken out. It’s the total sum you receive for your work before any of those other factors come into play.

3. Divide monthly debt by monthly income

When you divide all your monthly debt payments by your gross monthly income, you end up with a decimal number. If you shift this decimal point two places to the right, you get your debt-to-income (DTI) percentage.

For instance, consider Mr. John, who is excited about buying her first home. Her gross monthly income is $5,000, and his monthly debts include a $300 car loan, $100 for minimum credit-card payments, and $400 for student loans. John’s DTI ratio would be 16% ($800 / $5,000 = 0.16). With a low DTI ratio like this, he’s likely to be seen favorably by mortgage lenders.

However, remember that the lender will also consider the potential monthly payment of the loan you’re aiming for as part of your DTI. This can limit the amount you’re eligible to borrow.

Let’s say John is looking to secure a $300,000 mortgage at a 6% interest rate, resulting in a monthly mortgage payment of around $1,800. If we add this new payment to John’s existing debts, his DTI jumps to 52%. Invariably, this increase might affect his eligibility for the $300,000 mortgage he initially had in mind.

Normally, it’s important to understand how your DTI ratio impacts your borrowing capacity and how lenders assess your financial stability when considering your mortgage application.

Example for Debt-to-income Ratio Calculation

Different loan options and lenders have varying limits for the debt-to-income (DTI) ratio. To compute your DTI, simply sum up all your monthly debt payments and divide that figure by your gross monthly income. Gross monthly income is typically your earnings before any taxes or other deductions are taken away.

For example, let’s illustrate with numbers: If your monthly mortgage costs you $1,500, you have an additional $100 monthly for an auto loan, and $400 more for other debts, your combined monthly debt payments amount to $2,000 ($1,500 + $100 + $400 = $2,000). Suppose your gross monthly income is $6,000, then your debt-to-income ratio would stand at 33 percent ($2,000 is 33% of $6,000).

Conclusion

Remember that this ratio provides an insight into how much of your income is tied up in debt payments. It’s a very important factor lenders consider when assessing your eligibility for different loans, especially mortgages.

Different loan products and lenders also have their own thresholds for what is considered an acceptable DTI ratio.

Lastly, try your best to understand and calculate your DTI, so that you can gain valuable insight into your financial situation and how it aligns with potential borrowing opportunities.

Helpful Mortgage Insights

- Best Strategies to Improve Your Credit Score from 500 to 800

- Credit Score Check, Reports and Highest Range in Your Finance

- How to Remove Repossession Report Out of Your Credit Report

- Repo: How Long Does a Repossession Affect Your Credit Score?

- Repossession Law and its Consequences on Your Credit Report

- Can I Get a Home or Car Loan with a Repossession on my Credit?

- Home Equity Lines of Credit (HELOCs) What it is and How to Access it

- What is Credit Facility? How it Works for Personal & Business Loan and Mortgage

![9 Best Retirement Plans for Salary Jobs and Business Owners [Explained]](https://hybridcloudtech.com/wp-content/uploads/2023/03/9-Best-Retirement-Plans-for-Salary-Jobs-and-Business-Owners-Explained-100x70.png "9 Best Retirement Plans for Salary Jobs and Business Owners [Explained]")