Many people may want to ask; what does debt-to-income ratio mean for mortgage borrowers? A good debt-to-income ratio is 36% or lower. Your DTI is like a financial stability, showcasing your financial performance. If you’re applying for a mortgage, you must understand your Debt-to-income Ratio. Why? It’s a very important criteria that mortgage buyers use to understand your ability to navigate through loan repayments.

The Debt-to-income Ratio (DTI) is a formula that compares your monthly debt payments (like credit cards, student loans, and more) to your monthly income. It is like a back door that lenders use to uncovers your financial capability. Meaning that it is an important factor that shows the lenders your ability to pay back a loan.

So, why does it matter? Well, lenders want to see that you’ve got enough income to comfortably handle your debts without breaking a sweat. It’s like making sure your financial records are in sync with your paycheck.

Key Points about Debt-to-income Ratio

As you prepare for your mortgage journey with the information in this guide, remember that your DTI is your financial reputation. A healthy DTI can be your ticket to mortgage success, so keep those financial history healthy with good credit score. As we continue, note that these points below are important:

- Debt-to-income ratio (DTI) is a metric used by lenders to see how much of your income goes toward debt payments.

- A good DTI is generally around 36% or less, but you may qualify for a mortgage with a ratio up to 50%.

- You can lower your debt-to-income ratio by paying down your debt balances or increasing your income.

What is Debt-to-income Ratio?

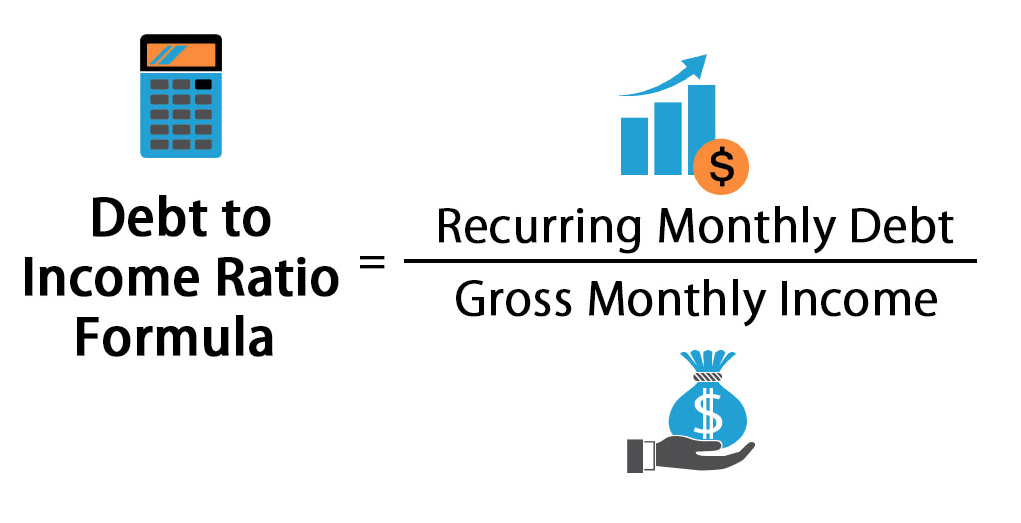

Your debt-to-income ratio is the calculation that show how much debt you pay each month in relation to your gross monthly income. Furthermore, it measures the amount of money you spend on debts each month compared to how much you bring home before taxes.

Why does it matter? Well, when a lender gives the you an application form for a mortgage, they want to be sure you’ve got the financial stability to comfortably repay that loan. It’s like making sure your income is enough to support your mortgage payment with ease. So, they review your DTI to make sure your debts aren’t stealing the spotlight from your income.

Calculating your DTI is as easy as ticking a financial records. You gather all your monthly debt payments – (those loans and credit card dues) – and sum them up. Then, you divide this sum by your gross monthly income. And remember, “gross” means your income before tax.

Imagine you’re in five-man panel defending your financial records. Your debt payments are your records you will show them, and your gross income is the guides you use to explain. The goal is to show that your income can cover your loan. There’s more information in the links below;

- Eligibility Requirements to Qualify for Mortgage: Minimum Credit Score, Down payment, and Debt levels

- Best Mortgage Home Loan to Choose from Conventional, Government FHA, Fixed or Adjustable Rate

Video explaining Debt-to-income Ratio for Mortgage Borrowers

Two types of Debt-to-income Ratio (DTI)

There are two types of DTI (debt-to-income ratio). The first one, called the “front-end DTI,” reviews account statement of general expenses. It focuses on your housing-related expenses, like your mortgage payment, insurance, and taxes.

The second, known as the “back-end DTI (debt-to-income ratio),” is a review of account in details. It’s takes a close look at all your previous oe current debts – the mortgage, credit cards, student loans, and more – against your income.

1. Front-end debt-to-income ratio

This is the sum of your monthly housing expenses – think mortgage, property taxes, insurance, and any homeowners association fees. It’s like the spotlight on your home costs, compared to your income.

Now, pay attention because here’s the twist: certain government-backed loans not only check your total DTI but also keep an eye on your front-end DTI specifically. It’s like having two judges critiquing different parts of your financial dance.

2. Back-end debt-to-income ratio

This is full details of your accounts, including all your monthly debt payments. We’re talking mortgages, credit cards, car loans, and any other financial commitments that tap into your paycheck each month. It is the financial records of all the transactions that make up your money in your bank account.

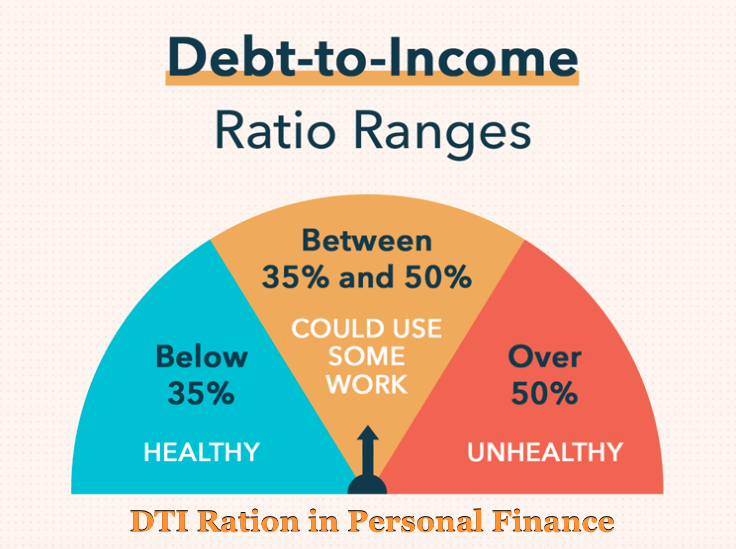

What is a good Debt-to-income Ratio?

Another important concept when it comes to loans is the DTI ratio, or Debt-to-Income ratio. Imagine this as a financial health check-up that lenders perform to see if you’re ready for that loan you’re applying for.

If you’ve got quite the pile of debts and you’re thinking about applying for new loans – be it a mortgage or any other type – your DTI ratio is vital in your application.

But what’s a good DTI ratio? Well, let’s put it this way: the lower, the better. Aim for a ratio around 36% or even less. Think of this number like your financial comfort zone.

Having a low DTI ratio is a positive criteria for loan approvals. It increase your chances of getting approved for a loan. Especially when we’re talking about mortgages, lenders usually decline if your DTI crosses the 50% mark. It’s like they’re saying, “Whoa, slow down there.”

So, if you want a DTI number to keep in mind, remember 36% or lower – that’s the best you can go. But don’t stress too much, because DTIs up to 43% are usually considered acceptable in the loan application.

Remember, lenders are like financial detectives. They want to make sure that you can handle your existing financial commitments while adding a new loan to the mix. So, when it comes to DTI, aim for that balance that keeps both you and your lenders happy!

Similar Posts

- Mortgage Calculator for Easy Debt Payoff with Formula

- How to Calculate Your Loan Payments with Mortgage Calculator

- Amortization Calculator – Schedule & Fixed Housing Interest Rates

- How Much is Mortgage Payments, Interest rate, Taxes and Insurance

What is the Best Debt-to-income Ratio for a Mortgage?

If you were to ask about what Debt-to-income Ratio is needed for a Mortgage, then you have to pay more attention here. This is to help you uncover the dynamics of DTI limits. Normally, the maximum DTI you can have solely depends on the type of mortgage you’re applying for as well as your financial profile.

Let me explain further: if you have a good credit score, you might just slide by with a slightly higher DTI. It’s like your financial reputation is doing the job for you.

Types of Mortgages

Now, let’s explain the basics for some of the most common types of mortgages out there. But note that, different lenders can be a bit like those teachers who expect extra homework – they might have stricter requirements.

So, buckle up for a quick tour of DTI thresholds for common mortgages, but always keep an eye out for those surprise twists from different lenders. Your financial profile is like a puzzle, and each piece matters!

1. Conforming Mortgage: 50%

The Conforming mortgages are the most popular type of mortgage. Now, when it comes to DTIs, it gives percentage of up to 50%. This is the highest DTI you can have and still have the approval from the the government-sponsored entities (Fannie Mae and Freddie Mac). They are the ones who lay down the rules for conforming mortgages.

Your specific mortgage application, including your credit score and down payment, can make you not to qualify for a loan. It’s like your personal factors coming into play. You see, not everyone can exceed that 50% line. Some borrowers might have to approve within a tighter range, like a DTI of 36% or 45%.

So, while 50% might be the perfect number on the conforming mortgage, your own financial stability could play a different role. Just remember, your loan approval chances wholly depends on your unique financial records!

2. FHA mortgage: 43%, but may be higher with compensating factors

Officially, to get an FHA mortgage, you need to have your back-end DTI (that’s the one including all your debts) under 43%. The Department of Housing and Urban Development (HUD) adds another rule to it – they’ve set a front-end ratio cap of 31%. That’s like saying your monthly mortgage payment, plus all those extras like taxes and insurance, can’t exceed the 31% mark, even if your total debt is behaving below the 43% line.

FHA borrowers sometimes get a little easy. If your financial records as well as credit score are really good, you might be able to get an FHA mortgage with a front-end ratio of 40% and a back-end DTI of 50%. However, you might need to show that you’ve got some extra cash in the bank (that’s the cash reserves), or other impressive financial factors that make you shine. In some rare cases, you might even qualify with a back-end ratio as high as 57%.

So, whether it’s a carefully calculated debt-to-income ratio (DTI) at 43%, or at 50%, or a daring dance at 57%, FHA mortgages have their own requirements when it comes to DTI ratios. Just remember, the key to the FHA loan often lies in your overall financial stability.

3. VA mortgage: Varies by lender

When it comes to the debt-to-income ratio , the Department of Veterans Affairs (VA) doesn’t put a maximum DTI for loan guarantees like some of the other players.

If your DTI is above the 41% mark, the VA says, “Hold on a sec, let’s take a closer look.” It’s like a gentle reminder to tread carefully. The VA will scrutinize your mortgage loan application when DTI is above 41%.

But each lender in this lenders might have their own rules. Some might want you to stay below 41% before they can grant you that VA mortgage pass. Others might be more forgiving, letting you stay with a DTI of up to 50%.

So, whether it’s a cautious number below 41%, a good percentage of up to 50%, or somewhere in between, the VA mortgage DTI has its own requirements. Just remember, your lender’s requirements might be the guiding factor in your mortgage application. So, if you’re going to apply for a VA mortgage, stay in line with your lender’s DTI requirements!

4. USDA Mortgage: 41%

The USDA mortgages are a special pathway to homeownership. In this type of mortgage, the Department of Agriculture sets the rules.

So, for a USDA mortgage, think of it as a two-part mortgage laon system. Your front-end ratio, which is like your monthly housing costs, should keep its moves under 29%. Then there’s the back-end ratio, which includes all your debts – that should stay under 41%.

The Department of Agriculture might approve your loan if you’ve got a credit score of at least 680. If you have at least one compensating factor, (money for up to three months’ mortgage payments in the bank), they might allow some exception. In that case, your front-end ratio could go up to 32%, and your back-end ratio could go up to 44% for USDA loan.

And guess what? In some rare cases, if you’re really struggling, even a back-end DTI of up to 46% might not get you the opportunity for a USDA loan.

So, whether you’re elegantly having between 29% and 41% DTI, adding some numbers with a 32% front-end and 44% back-end duo, or even reaching for the top with a 46% back-end, USDA mortgages have their own Debt-to-income ration numbers. Just remember, it’s all about keeping the numbers to secure that USDA mortgage approval.

How to Calculate debt-to-income ratio for a Mortgage

Now, let’s talk about How to Calculate Debt-to-income Ratio for a mortgage application process.

1. List all your monthly debt payments

When we’re talking about your financial stability, there’s a list of basic responsibilities that you must be able to clear every month. They include payments for auto loans, student loans, mortgages, personal loans, child support and alimony, and, of course, those bank credit cards.

When it comes to those credit cards, we’re not looking at the spending you choose to make each month. Nope, it’s all about the minimum payment that’s expected from each of your cards. Think of this as the basic step that keeps the rhythm going.

But wait, there’s a guest list for the debt too. Household utility bills, health insurance, and car insurance, they’re like the cool kids hanging around, but they’re not considered part of the debt crew.

So, to sum it up, it’s like a meeting of financial partners – auto loans, student loans, mortgages, personal loans, child support, alimony, and the minimum credit card payments – all taking center stage in your monthly debt. The other everyday expenses – utility bills, health insurance, and car insurance are also there to influence your financial capabilities.

2. Find your gross monthly income

Your gross monthly income is like the big number – the total sum of money you make before those tax collectors come knocking. It’s like the total money before government taxes deduction. So, remember, when we’re talking gross, we’re talking the grand total, no deductions allowed!

3. Divide monthly debt by monthly income

When you want to figure out your Debt-to-Income ratio, it’s like a little math magic trick.

Step 1: You take all those monthly debt payments – the car loan, credit card payments, student loan bills – and add them up.

Step 2: Then, you divide this sum by your gross monthly income, which is your full paycheck before taxes.

That answer you get is a decimal, a fraction. Move that decimal point two places to the right, and you’ve got your DTI percentage. It’s like turning a fraction into a percentage.

For example, let’s join Stacy Jonathan on her homeownership journey. With a gross monthly income of $5,000, she’s got $300 for the car, $100 for credit cards, and $400 for student loans. So, her total debts sum up to $800. When we do the math ($800 / $5,000), Amelia’s DTI ratio is 16%.

If Stacy Jonathan wants to slide into a $300,000 mortgage at a 6% rate, that means a monthly payment of around $1,800. Add that to her other debts. Her DTI moves up to 52%.

So, the moral of the story, my friends, is that while Amelia might not be able to get into that $300,000 dream mortgage, understanding her DTI helps her make a financially stable decision. DTI ratios, is where math meets reality on your journey to homeownership.

How to lower your debt-to-income ratio for Mortgage Application

If you’ve checked the numbers and that DTI of yours is hanging out above that 36% line, it’s time to get into action mode before you march into the land of loans.

In order to lower your debt-to-income ratio, you have two options:

- Pay off more of your debt

- Earn more

Option 1: Make sure you pay off more of your debt. It’s like a debt showdown. You roll up your sleeves, pay more than the bare minimum on your debts. You can learn from the 11 Ways to Quickly Get Out of Debt and Rebuild Your Credit Score from my previous article. The goal here is to reduce those balances, making sure your debt does not take a large piece of your income. No taking out more debt, just a way to get of debt you already owe.

Option 2: It’s the “working more option” to increase your earnings. You aim to bring in more income. You might go to your boss and negotiate a higher salary. Or, you venture into the side gigs/jobs, picking up an extra hustle to fatten up that wallet.

When you pay-off-debt more by earning more money, your DTI starts to reduce. In a short time, the debt-to-income ratio percentage drops, and suddenly, you’ll have more advantage for loan applications.

In the bottom line, remember, when your DTI is giving you a run for your money, these steps – slashing debts and boosting earnings – are your best option. Once you’ve got that DTI down, you’re ready to put on your best financial foot forward and enter the loan application with confidence!

Debt-to-income ratio Frequently asked Questions

What is an acceptable debt-to-income ratio for a mortgage?

Rule number one: You can’t have a debt-to-income ratio above 50% DTI line. If you’re eyeing a mortgage, keep your DTI below 50% if you want a seat at the table (qualify for a mortgage).

Rule number two: If you’re aiming for the easier mortgage terms, aim for DTI of 36%. It’s like the sweet spot where lenders are all smiles.

Can you get a mortgage with 55% DTI?

Yes, possible – to get a mortgage with a DTI as high as 55%. But, here’s the catch – you need to bring your financial A-game (strong application). Think of it like building a fortress of financial strength.

Now, when we talk about this special deal, it’s like a secret gathering for government-backed mortgages. They’re like the exclusive club that might nod your way. Let’s take FHA loans, for instance. They’re known to potentially stretch their arms out to DTIs up to 57%.

How do I figure out my debt-to-income ratio?

When it’s time to tackle that DTI ratio, it’s as simple as a math class.

Step one: Grab all those monthly debt payments – the car loan, the student loan, the credit cards – and put them together.

Step two: Now, take that total sum and divide it by your gross monthly income. That’s like your paycheck before taxes swoop in to take their cut.

The result? It’s your DTI ratio, the magic number that tells you just how much of your income is dancing its way into those debt payments.

How can I lower my debt-to-income ratio quickly?

When you’re aiming to reduce that DTI ratio, there are a moves to consider.

Move one: Paying off a chunk of those credit card balances. It’s like shedding weight off your shoulders and, as a bonus, it slashes the amount you owe each month. Imagine it as a swift step toward a lower DTI ratio.

Move two: Make a debt consolidation loan. This is like assembling your debts into one package. Not only does it potentially lower the interest you’re working over, but it also trims down those monthly payments. It’s like streamlining your financial responsibilities.

Helpful Guides

- Best Strategies to Improve Your Credit Score from 500 to 800

- Credit Score Check, Reports and Highest Range in Your Finance

- How to Remove Repossession Report Out of Your Credit Report

- Repo: How Long Does a Repossession Affect Your Credit Score?

- Repossession Law and its Consequences on Your Credit Report

- Can I Get a Home or Car Loan with a Repossession on my Credit?

- Home Equity Lines of Credit (HELOCs) What it is and How to Access it

- What is Credit Facility? How it Works for Personal & Business Loan and Mortgage