![How Much is Mortgage Payments?Calculate using Interest rate, Taxes and Insurance [Online Calculator]](https://hybridcloudtech.com/wp-content/uploads/2023/06/How-Much-is-Mortgage-PaymentsCalculate-using-Interest-rate-Taxes-and-Insurance-Online-Calculator.png "How Much is Mortgage Payments?Calculate using Interest rate, Taxes and Insurance [Online Calculator]")

Do you know how to calculate your mortgage payments using the mortgage formula or mortgage calculator? As a law abiding citizen, how much will you pay in interest on my mortgage over 30 years of my life? This is a serious question to ask yourself before taking a home mortgage loan. A simple mortgage calculator can help you calculate how much you will pay in interest rate, Taxes and Insurance.

We all know that an affordable mortgage reduces financial stress. It can also help you to plan ahead of the future, plus getting you ready for any emergency expenses that may arise unexpectedly.

However, when it comes to calculating your mortgage payments, several factors come into play. These factors include the loan amount, interest rate, and loan term. Understanding these factors allows you to make informed decisions about your mortgage, considering the impact they have on your monthly payment obligations.

I will break these mortgage factors down for better understanding while you focus carefully to this helpful guide on how much is Mortgage Payments.

What is a Mortgage in Layman’s Understanding?

A mortgage is a long-term commitment that typically lasts for several years. It is perfectly understandable to desire a sense of financial security and peace of mind without constant concerns about meeting your mortgage payments. For you to achieve this, you have to create a comfortable payment plan that aligns with your financial capabilities and resources. If you are able to ensure that your mortgage payments are within your means, you can effectively manage your finances and approach your mortgage with confidence and stability.

Factors that Impact Mortgage Payment

When calculating your mortgage payments, several factors come into consideration. These factors include the loan amount, the interest rate applied to your loan, and the loan term. Generally, the more you owe and the higher the interest rate, the higher your monthly payments will be. Bear in mind that there are 3 ways the President could Impact Social Security in United States while you are buying a home.

Additionally, if you choose to include funds for taxes and insurance in your monthly payment, it’s known as escrow in the finance sector. This ensures that these expenses are covered regularly. However, including escrow in your payment will increase the overall amount you need to pay each month.

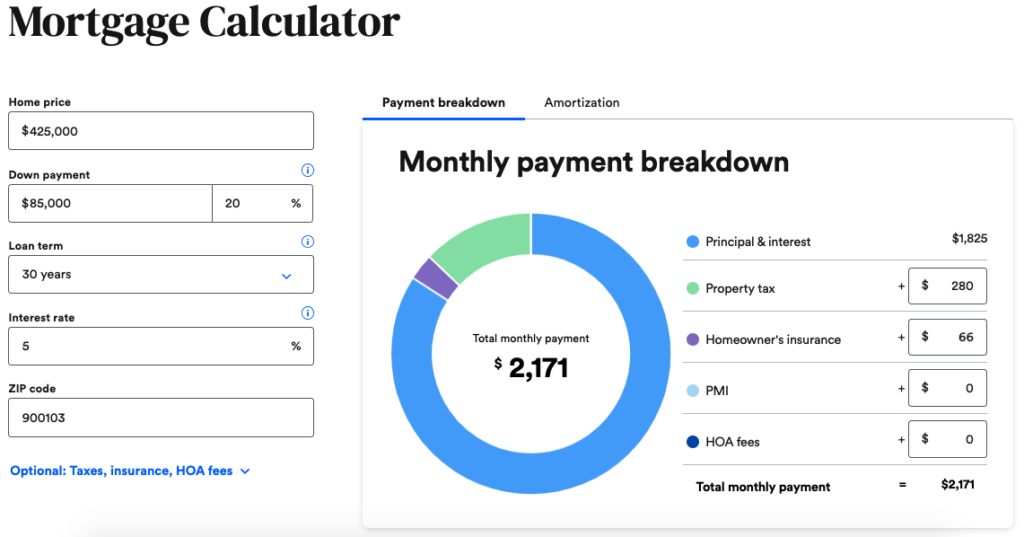

Online Calculators

Fortunately, there are simple online calculators available online. These bank rate mortgage calculators can help you in determining the payment amount that suits your situation best. These online calculators consider all the factors we mentioned earlier and assist you in determining an optimal payment amount that fits well within your budget and aligns with your financial objectives.

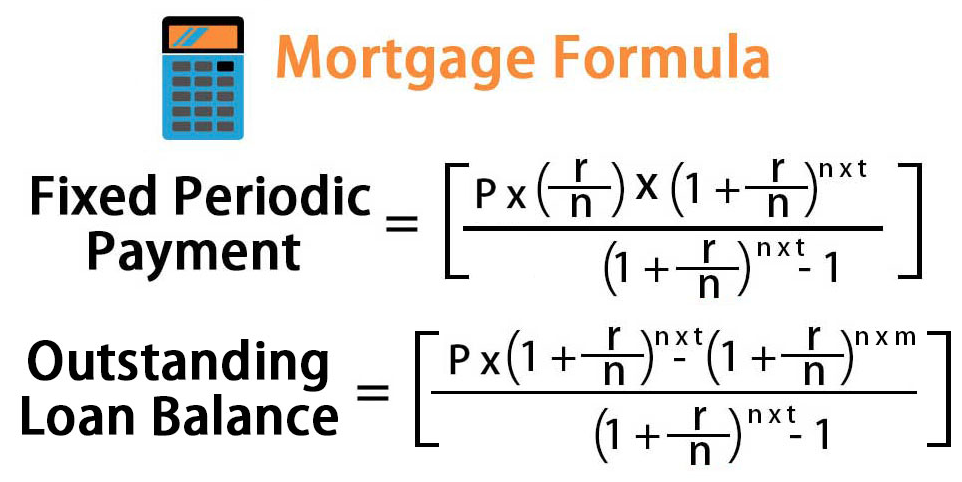

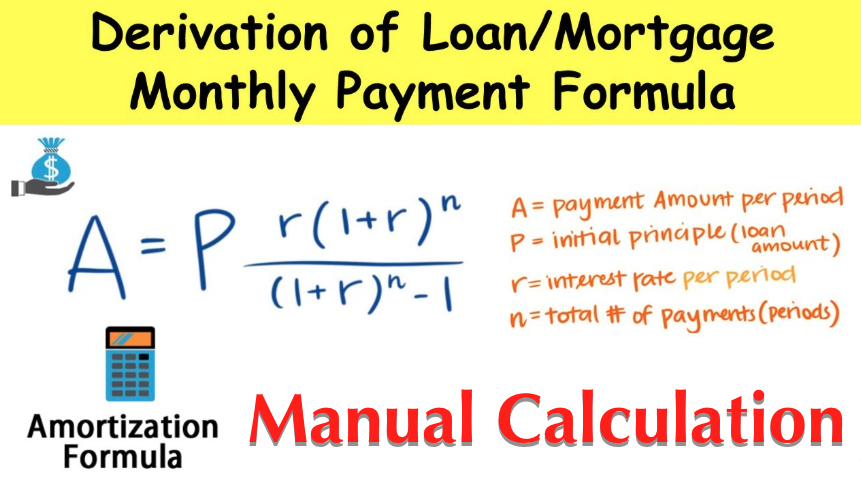

Mortgage Formula?

What is Mortgage Formula? The calculation of a mortgage revolves around two main elements: the fixed monthly payment and the outstanding loan amount.

The fixed monthly mortgage repayment is determined using the annuity formula, which is a mathematical representation of the calculation.

Fixed Monthly Mortgage Repayment Calculation = P * r * (1 + r)n / [(1 + r)n – 1]

where P = Outstanding loan amount, r = Effective monthly interest rate, n = Total number of periods / months

On the other hand, the outstanding loan balance after payment m months is derived by using the below formula,

Outstanding Loan Balance= P * [(1 + r)n – (1 + r)m] / [(1 + r)n – 1]

How does Free Online Calculator Help You (Advantages)?

There are free calculators online to help you find your ideal payment amount. Just use any free online calculators, you can gain a clearer understanding of how different loan amounts, interest rates, and loan terms impact your monthly payments. This knowledge gives you powers to make better decisions and find a payment amount that you can comfortably afford. Finally, it will allow you to stay on top of your mortgage payments without unnecessary stress.

How the Mortgage Loan System Works [Explained]

When you take out a mortgage, it means you borrow money from a lender to buy a house or property. Now, paying off a mortgage takes many years, and it’s important to make sure the payments are manageable for you so that you don’t stress about them all the time.

To stay on top of your mortgage payments, it starts with having a payment plan that you can comfortably afford. This means considering several factors that affect your payments. These factors include the amount of money you borrowed (the loan amount), the interest rate charged by the lender, and the length of time you have to repay the loan (the loan term).

If you borrow a larger amount or have a higher interest rate, your monthly payments will be higher. Additionally, if you choose to include escrow, which is a portion of your payment set aside for taxes and insurance, that will also increase your monthly payment.

To help you figure out the ideal payment amount that fits your budget, there are free calculators available online. These calculators take into account all the variables we discussed earlier, allowing you to input your loan details and calculate what your monthly payments would be.

Notice that if you are using these online calculators, you can better understand how different loan amounts, interest rates, and loan terms impact your payments. This way, you can find a payment amount that suits your financial situation and ensures that you can comfortably manage your mortgage payments without undue stress.

Helpful Resources:

- 10 Type of Banks and Financial Institutions – Local & International

- How to Consolidate Credit Card Debt without Hurting your Credit

- How to Borrow Money with Instant Cash Advance from your Credit Card

Total Amount Financed

The amount you finance after making your down payment will significantly impact your monthly mortgage payment. It is advisable to contribute as much as you comfortably can towards the down payment without depleting your savings entirely.

It’s important to maintain funds in your savings account to cover unexpected expenses such as emergency repairs, fluctuations in income, and other unforeseen circumstances. Avoid using all of your available funds to purchase your home, as this could leave you without any savings for emergencies. Striking a balance between down payment and savings will provide you with financial security and peace of mind.

If your objective is to reduce your mortgage burden, it is advisable to contribute a larger down payment if you have the available funds. Doing so will not only lower the principal amount you borrow but also decrease the overall interest you pay over the duration of your mortgage loan.

Conversely, if you make a minimal down payment, your monthly payments will be higher. Therefore, putting down a larger sum can help you save on interest and potentially lower your monthly payment amounts in the long run.

Interest Rate

If you can get a lower interest rate for your mortgage loan, you will have to pay less money each month. Having good credit is important for getting the best rate. Do not forget that Poor Credit Score can Hurt your Social Security Benefits. Also note that the rates for home loans can change because of the economy. It’s a good idea to apply when the rates are low. If you already have a mortgage with a high interest rate, you might want to think about refinancing. Refinancing could help you get a lower interest rate and make your mortgage payments smaller.

There are two types of interest rates you can have for your mortgage: fixed or variable. With a fixed rate, you know the exact amount of interest you will pay throughout your entire mortgage agreement. This can be beneficial because it means your payment amount will stay the same, and you won’t have to worry about it increasing significantly if interest rates go up.

If you have a variable interest rate for your mortgage, it can fluctuate over time. Sometimes it may go down, resulting in a decrease in your payment amount, which can be beneficial. However, it can be challenging to budget for an increased payment if the interest rate goes up. It’s important to be prepared for potential changes in your monthly payment and consider the impact on your budget when opting for a variable interest rate.

Length of the Loan

Typically, home loans are structured for a duration of 30 years, but you have the flexibility to choose a shorter repayment term. Options like 10-year and 15-year loans are available. The choice of loan term depends on the total amount you borrow and what you can comfortably afford to pay.

It’s important to consider your income and expenses when deciding on the loan term. Longer loan terms result in smaller monthly payments, but it’s worth noting that you will end up paying more interest over the life of a 30-year loan compared to a 15-year loan.

Ultimately, the decision between loan terms involves finding the right balance between affordable monthly payments and minimizing the total interest paid over the loan’s duration.

If you decide to choose a longer loan period, it’s important to ensure that your loan does not have any pre-payment penalties. This means that you won’t be charged any fees for paying extra towards your loan when you have additional funds.

Trust me, if you continue making extra payments towards your loan when you have the ability to do so, you can effectively pay off your home faster. While it’s not mandatory to make these additional payments, doing so can help you build equity and ultimately own your home outright in a shorter period of time. It’s a good idea to check the terms of your loan agreement and consult with your lender to understand if there are any restrictions or penalties associated with pre-payments.

How to Pay Extra for Loan Payment

There are 6 best ways to pay extra towards the loan easily. They include:

- Bonuses from work

- Inheritance or gifts

- Investment dividends

- Overtime earnings

- Stimulus funds

- Tax return funds

You mayAlso Like this

- The Role of The Attorney General in Taxation and Tax-Related Matters

- House Mortgage – Meaning, Types, Loans and How it Works

- Perfection of Legal Mortgage in Nigeria Law & Procedure for Loan Property

Escrow for Taxes and Insurance

When you finance a home, it is necessary to have insurance coverage. The specific amount of coverage and the details included in the policy can vary. You need to meet the requirements set by the lender and the regulations in the area where the home is located. You can choose to pay for insurance annually using your own funds. Similarly, you also have to pay annual taxes for the house.

Paying a lump sum annually for insurance and taxes can be challenging for your budget. That’s why many homeowners prefer to include these costs in their monthly mortgage payments. While this increases the monthly payment amount, it eliminates the need to come up with separate funds for insurance and taxes, making it more convenient to manage homeownership costs.

If you choose to include taxes and insurance in your mortgage payment, the funds are placed in an escrow account. Your lender will estimate the total amount you will need to pay for insurance and taxes throughout the year. They will then divide this amount by 12 months and set aside a portion of your monthly payment into the escrow account on your behalf. This ensures that there are sufficient funds available when the insurance and tax payments are due.

When the insurance and tax bills become due, the lender will withdraw the necessary funds from the escrow account and make the payments on your behalf. If there are any surplus funds in the escrow account, the lender will refund them to you and adjust the account for the following year. On the other hand, if there aren’t sufficient funds in the escrow account to cover these expenses, your monthly mortgage payment may increase slightly to prevent such a shortfall in the future. Lenders are experienced in estimating these costs accurately, so you need not worry too much about fluctuations within the escrow account.

Online Calculators for Calculating Mortgage Payment

You can use free online calculators to determine your mortgage payments. It will help you get correct figures. It’s a good idea to input slightly higher amounts to account for any potential changes. For instance, if you’re considering a home between $200,000 and $250,000, enter the higher value of $250,000. Enter the interest rate that you have been approved for or have pre-qualified for.

For you to get an estimate of the average cost of insurance and taxes for a home, you can research typical rates in your area or consult with insurance providers and local tax authorities. By including these costs in your calculations, you can get a better idea of your total mortgage payment. You can also adjust variables, such as the down payment amount, to see if increasing it lowers your monthly payment enough to fit within your desired payment range.

If the online tools indicate that the mortgage payment for a home priced at $250,000 is too high for your budget, you can explore different scenarios to make it more manageable. Consider adjusting the home price to a lower amount, such as $180,000 or $200,000, and see how it impacts your monthly payment. Taking the advantage to lower the purchase price, you may find a payment amount that aligns better with your financial comfort zone.

In summary, for you to makesure you can comfortably manage your monthly mortgage payment, it’s crucial to stick within your preferred price range. If you feel more comfortable with a lower figure, focus your search on homes within that price range. Maintaining a mortgage payment that aligns with your financial capacity is essential to avoid potential financial difficulties or the risk of foreclosure. It’s always better to be cautious and choose a home that fits well within your budget.

- Top 10 Ways to Prepare for Retirement as a Civil Servant or Private Worker

- 9 Best Retirement Plans for Salary Jobs and Business Owners [Explained]

- Retirement Planning Guide: 10 Safest Places in the World To Retire

- House Mortgage – Meaning, Types, Loans and How it Works

- 11 Best Stock Trading Platforms + Apps in the World for Beginners and Pro

![9 Best Retirement Plans for Salary Jobs and Business Owners [Explained]](https://hybridcloudtech.com/wp-content/uploads/2023/03/9-Best-Retirement-Plans-for-Salary-Jobs-and-Business-Owners-Explained-100x70.png "9 Best Retirement Plans for Salary Jobs and Business Owners [Explained]")

: What is Adjustable Mortgage Rates?")