What is the Definition of Credit Reference

By definition, a credit reference is a document or piece of information used by lenders, creditors, or financial institutions to assess a person’s or a company’s creditworthiness. It provides an idea of an entity’s financial behavior and history, helping lenders make informed decisions about extending credit, loans, or other financial services.

Credit references typically include details about the applicant’s borrowing and repayment history, outstanding debts, credit limits, and overall financial behavior. They help lenders gauge the level of risk associated with lending money or extending credit to the applicant. There are some Difference Between FICO Score and Credit Score in loan financing and creditworthiness.

Credit Reference Explanation

Credit reports from major credit bureaus are commonly used as credit references for people. These references can also include documents showing assets, along with letters from past lenders and personal or business contacts. Not only lenders, but landlords also often ask for credit references when considering potential tenants.

With that explained, that covers the definition of a credit reference. Now, let’s move on to understanding the different types of credit references and how they function.

Important Finance Guides

- Remove Repossession Report Out of Your Credit Report to Boost Your FICO

- When does Capital One Report to Credit Bureaus about your Credit Score?

- Is it Possible to Get Home Loans with Bad Credit with Multiple Options?

Examples and Types of Credit References in Finance

Let us elaborate on the types of credit references, specifically credit reports, asset documentation, and reference lenders. Credit references play a vital role in financial transactions and lending decisions. I will give you a breakdown of how these three common types of credit references work:

- Credit Reports

- Asset Documentation

- Letter of Reference

Now, lets discuss them in full details for better understanding.

1. Credit Reports:

Local banks and various other lenders usually ask for a person’s credit report when they apply for credit, like a loan or a credit card. These reports are provided by three major credit bureaus: Equifax, Experian, and TransUnion. The reports show details about an individual’s credit usage, such as their owed amount and whether they pay on time. Lenders, landlords, employers, and other businesses buy these reports from the bureaus.

These bureaus gather information mainly from current and past creditors of the person. Because not all creditors give information to all three bureaus (some may not share at all), credit reports can differ between bureaus. This is why lenders might check multiple reports, especially for significant loans like mortgages.

The data in credit reports is used to calculate credit scores, using formulas developed by FICO Score and VantageScore. Credit scores, often requested by lenders and others, aren’t included in credit reports but can be obtained from the same sources.

Related: What are the 5 Factors That Affect Your Credit Score?

A credit report is a comprehensive document that outlines your credit history or a business’s credit history and financial behavior. It includes information such as:

i) Credit Score:

A numerical representation of creditworthiness, calculated based on factors like payment history, outstanding debts, length of credit history, types of credit, and recent credit inquiries

ii) Payment History:

Details of credit accounts, loans, and credit cards, along with records of on-time payments, late payments, and defaults.

iii) Credit Inquiries:

A list of entities that have accessed the individual’s credit report, categorized as hard inquiries (initiated by the individual for credit applications) and soft inquiries (initiated for background checks or pre-approvals).

iv) Debt Accounts:

Information about existing loans, credit cards, mortgages, and other credit facilities, including balances and payment schedules.

v) Public Records:

Any legal actions or public records related to bankruptcy, tax liens, or other financial issues.Credit reports provide lenders and creditors with an overview of an applicant’s financial behavior and help them assess the level of risk associated with extending credit.

2. Asset Documentation:

Asset documentation involves providing evidence of owned assets, which can be used as collateral or as proof of financial stability. Although credit reports contain a wealth of information, there are certain details they don’t include. This includes any information about a person’s assets or income.

So, if a creditor wants to know how much money someone has in the bank or the investments they own, the person would need to provide this separately. Usually, this is done through account statements from financial institutions. As for verifying income, they might need to show their pay stubs and/or income tax returns. These assets might include:

i) Real Estate:

Property deeds, mortgage agreements, and assessments of property value.

ii) Vehicles:

Ownership documents for cars, trucks, or other vehicles.

iii) Investments:

Documentation of stocks, bonds, retirement accounts, and other investment holdings.

iv) Savings and Bank Accounts:

Statements from bank accounts or savings accounts.

v) Valuables:

Proof of ownership of valuable items like artwork, jewelry, or collectibles.

Asset documentation serves to demonstrate the applicant’s ability to cover debts and financial obligations, providing assurance to lenders in case of default.

3. Letter of Reference Lenders:

Reference lenders are people or entities that have previously lent money to or have had financial transactions with the applicant. They can provide insights into the applicant’s borrowing behavior, payment reliability, and overall financial responsibility. Reference lenders may be contacted by the current lender as part of the credit assessment process.

In an effort to strengthen their argument for being a suitable candidate for a loan (or a rental apartment), the person applying might consider asking for reference letters from past lenders, previous landlords, or even people who are familiar with them. These letters usually confirm the person’s ability to handle credit and sometimes speak about their qualities, like honesty, diligence, and dependability, along with how long the letter writer has known them.

Reference lenders might provide information about the applicant’s:

i) Loan Repayment History:

Whether the applicant made payments on time and met their financial obligations.

ii) Credit Behavior:

How the applicant managed credit facilities, loans, or credit cards in the past.

iii) Trustworthiness:

The applicant’s reliability in terms of financial commitments.Reference lenders contribute to the lender’s understanding of the applicant’s creditworthiness and risk profile.

Summary

In summary, credit reports, asset documentation, and reference lenders collectively help lenders make informed decisions about extending credit, assessing the applicant’s financial stability, and managing potential risks associated with the lending relationship.

See: Credit Score Check, Reports and Highest Range in Your Finance

Credit Reference for Personal account

The Credit Reference for single or personal account, a credit reference often includes:

- Credit Score: A numerical representation of an individual’s creditworthiness, based on their credit history, outstanding debts, payment history, and other financial factors.

- Credit Report: A comprehensive report detailing an individual’s credit history, including past and current loans, credit card accounts, payment history, and any late payments or defaults.

- Debt Obligations: Information about existing debts, outstanding balances, and monthly payments on loans, credit cards, mortgages, and other credit facilities.

- Payment History: Records of on-time payments, late payments, and missed payments on credit accounts.

- Public Records: Any legal actions or public records related to bankruptcy, tax liens, or other financial issues.

- Credit Inquiries: A list of entities that have accessed the individual’s credit report, often categorized as hard inquiries (initiated by the individual’s credit application) and soft inquiries (initiated for background checks or pre-approvals).

Credit Reference for Business

Then, for businesses, a credit reference may include:

- Business Credit Score: Similar to an individual credit score, this score reflects the creditworthiness of a business based on its financial history and payment behavior.

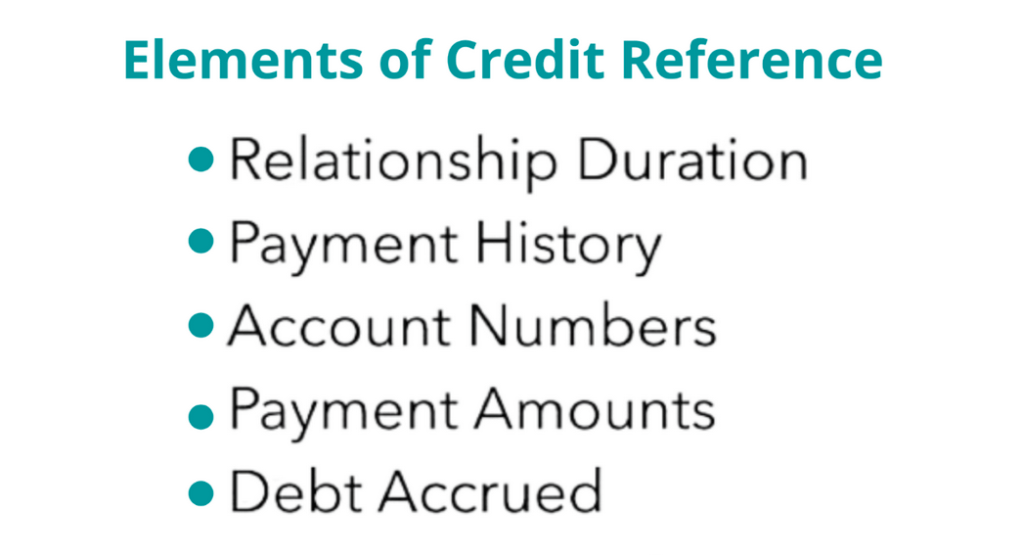

- Trade References: Information about the company’s relationships with suppliers, creditors, and vendors, including credit terms and payment history.

- Financial Statements: Documents such as income statements, balance sheets, and cash flow statements that provide insights into the financial health of the business.

- Business History: Details about the company’s establishment date, ownership structure, and industry.

- Banking Relationships: Information about the company’s banking history, including any lines of credit or loans it may have.

Lenders and creditors use credit references to make decisions about whether to approve credit applications, set credit limits, and determine interest rates. It’s crucial for individuals and businesses to maintain a positive credit history by making timely payments, managing debts responsibly, and keeping their credit references accurate and up-to-date.

Helpful Guides

- What is the Best Credit Score Needed for Me to buy a House or car?

- 11 Ways to Quickly Get Out of Debt and Rebuild Your Credit Score

- Bad Credit Score: How Does it Affect Your Credit Loan Application

- Rebuild Your Credit Score After Repossession for Missing Payments

- Repo: How Long Does a Repossession Affect Your Credit Score?

- Best Strategies to Improve Your Credit Score from 500 to 800

- How Can Poor Credit Score Hurt My Social Security Benefits?