Let’s talk about factors that affect your Credit Score. Have you been asking about the factors that impacts your credit scores? Do you ever think that understanding what affects your credit score requires a Harvard degree? Well, guess what? It’s actually pretty easy. You don’t need to be an expert. Let me break it down for you in simple terms.

Credit scores, which usually range from 300 to 850, are determined by considering five key factors. Lenders use these scores to assess the possibility of you repaying your debts, making them important in determining whether you qualify for a new loan.

As your financial situation develops your credit score can also change. Understanding the factors and types of accounts that affect your credit score provides you with an opportunity to improve it gradually

Top 5 Credit Score Factors

Different scoring models may have slight contrast in their criteria, but the following are the most common factors that affects your credit scores:

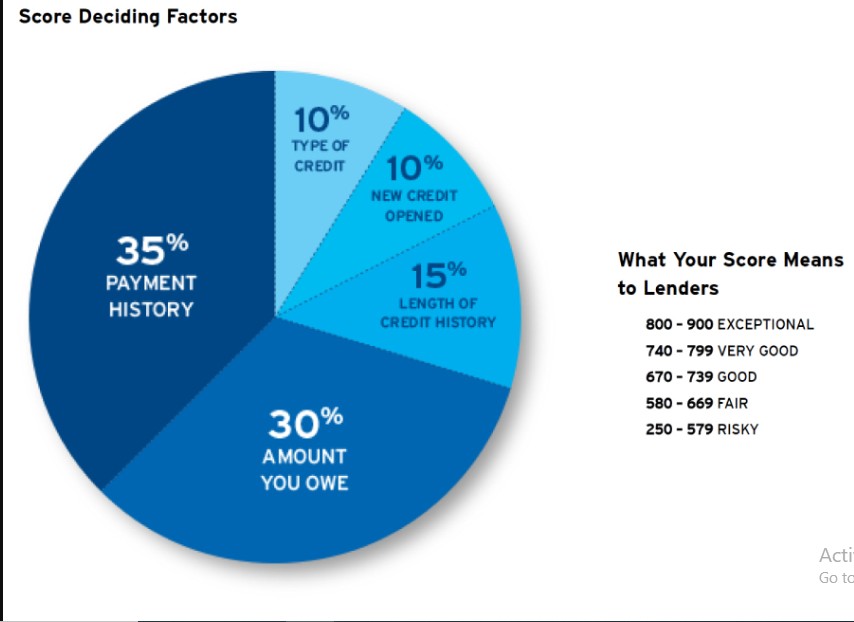

Payment history:

This is the most crucial factor in credit scoring. Even a single missed payment can negatively impact your score because lenders want to ensure you repay your debts in time. It contributes to 35% of your FICO Score, which is mostly use 90% by top lenders.

The amounts you owe:

Specifically, your credit utilization ratio, are the next significant aspect affecting your credit scores. Your credit utilization ratio compares your current credit usage to your total credit limits. Using over 30% of your available credit is seen negatively by creditors. This factor accounts for 30% of your FICO® Score.

The length of your credit history:

This also makes up 15% of your FICO Score. As it includes the age of your oldest and newest credit accounts, as well as the average age of all your accounts. Generally, having a longer credit history agrees with higher credit scores.

Credit mix is also taken into account:

Contributing 10% to your FICO® Score. Having a different range of credit accounts, such as car loans, credit cards, student loans, mortgages, etc., indicates your ability to handle various types of credit products.

Lastly, new credit activity:

This influences 10% of your FICO Score. Opening multiple credit accounts or having numerous hard inquiries from lenders when you apply for credit can indicate increased risk negatively affect your credit score.

Types of Accounts That Affect Credit Scores

Credit files usually contain information about two main types of debt: installment loans and revolving credit. These types of accounts play a important role in determining your credit scores because they maintain a record of your debt and payment history. By accessing how you handle these accounts, credit scoring models assess your creditworthiness.

Installment Credit:

Involves loans where you borrow a specific amount and agree to make monthly payments until the entire loan is repaid. Examples of installment accounts include student loans, personal loans, and mortgages.

Revolving credit:

This is commonly associated with credit cards but can also include certain types of home equity loans. With revolving credit, you have a predetermined credit limit, and you make minimum monthly payments based on the amount of credit you use. Unlike installment credit, revolving credit can vary over time and does not have a fixed repayment term.

How Does Having Various Accounts Affect Your Credit Score?

How Having a Variety of Accounts Affects Your Credit Score. The mix of credit accounts you have plays a significant role in calculating your credit scores, but it’s often overlooked by consumers.

Having different types of credit accounts, such as a mortgage, personal loan, and credit card, demonstrates to lenders that you can effectively handle various forms of debt simultaneously. It also provides them with a clearer understanding of your financial situation and ability to repay debts.

While having a less diverse credit portfolio won’t necessarily cause your scores to decrease, it’s generally advantageous to have multiple types of credit accounts as long as you make timely payments. Credit mix contributes 10% to your FICO Score and can have a meaningful impact on achieving a high score.

Can Service Accounts Affect Your Credit Score?

Service accounts, such as utility and phone bills, are not automatically included in your credit file, meaning they don’t typically affect your credit score unless they go to collections due to nonpayment. However, there is a new innovative tool called Experian Boost that allows users to benefit from their on-time utility and telecom payments.

If you choose any reliable credit agent, you can instantly increase their FICO Score by connecting their bank accounts and confirming their eligible payment history. This platform is currently the only way to receive credit for utility and telecom payments.

By verifying and adding utility and phone bill data to their credit file, you can see an immediate boost to their FICO Score. It’s important to note that late payments on utility and telecom bills don’t affect your Boost score. However, if an account goes to collections due to nonpayment, it will remain on your credit report for seven years.

What Can Hurt Your Credit Scores?

As mentioned earlier, specific aspects of your credit file have a remarkable impact on your credit score, and certain actions can have negative consequences. Here are some common actions that can hurt your credit score:

Missing payments:

Your payment history is important for your FICO Score. Even a single late payment or missed payment can negatively impact your score.

High credit Utilization:

Using a significant portion of your available credit can raise concerns among lenders. Aim to keep your credit utilization below 30%, with lower percentages being even better. Credit utilization accounts for 30% of your FICO Score.

Multiple credit applications:

Each time a lender request for your personal credit report, it creates a hard inquiry on your file. These inquiries can lower your score temporarily. Having too many inquiries within a short period can indicate financial burdens or difficulty obtaining new credit.

Defaulting on accounts:

Negative account information like foreclosure, bankruptcy, repossession, charge-offs, and settled accounts can have a severe and long-lasting impact on your credit. These negative marks can affect your credit for several years, sometimes up to a decade.

How to Improve Your Credit Score to 750

To improve your credit score is easy once you understand why your score is struggling. This sometime takes time and effort, but developing responsible habit can help you grow your score in a long run.

First step to get a free copy of your credit report and score so you can understand what is in your credit file. Next, you should also focus on what is bringing your score down and work toward improving these areas.

Below are some steps you can take to increase your credit score.

- Pay your bills on time. Because payment history is the most important factor in making up your credit score, paying all your bills on time every month is critical to improving your credit.

- Pay down debt. Reducing your credit card balances is a great way to lower your credit utilization ratio, and can be one of the quickest ways to see a credit score boost.

- Make any outstanding payments. If you have any payments that are past due, bringing them up to date may save your credit score from taking an even bigger hit. Late payment information in credit files include how late the payment was—30, 60 or 90 days past due—and the more time that has elapsed, the larger the impact on your scores.

- Dispute inaccurate information on your report. Mistakes happen, and your scores could suffer because of inaccurate information in your credit file. Periodically monitor all your credit reports to make sure no inaccurate information appears. If you find something that’s out of place, initiate a dispute as soon as possible.

- Limit new credit requests. Limiting the number of times you ask for new credit will reduce the number of hard inquiries in your credit file. Hard inquiries stay on your credit report for two years, though their impact on your scores fades over time.

Related Posts

- Recommendation Letter Templates for Job Application, School Admission

- How to Write a Letter of Query to Staff: Misconduct, Absent, Lateness

- How to Respond to Query Letter given by Employer at your Workplace

- Loan Approval Letter from Employer to Employee [Sample Template]

- Best Reply to Query Letter for Fighting at Workplace – Apology Letter

- Letter to Explain Why Disciplinary Action Should Not be Taken Against You

What to Do if You Don’t Have a Good Credit Score?

To establish and build your credit when you don’t have a credit score, consider the following options:

1. Get a secured credit card:

A secured credit card works similarly to a regular credit card, but it requires a security deposit equal to your credit limit when you sign up. By using the secured card for small essential purchases and consistently paying your bill in full and on time, you can establish and build your credit history. You can do more research online to learn more about how secured cards work and browse Experian’s secured card partners. This will go a long way to mitigate some factors that affect your Credit Score.

2. Become an authorized user:

If you have a close relationship with someone who has a credit card, you can ask them to add you as an authorized user. As an authorized user, you’ll receive your own card and have spending privileges on the primary cardholder’s account.

In many cases, credit card issuers report authorized users to the credit bureaus, which can contribute to your credit file. If the primary cardholder makes all their payments on time, it can have a positive affect on your credit.

Want to instantly increase your credit score?

Companies like Experian, TransUnion and Equifax helps you simply by giving you credit for the utility and mobile phone bills you’re already paying. Until now, those payments did not positively affect your scores.

This service is completely free and can boost your credit scores fast by using your own positive payment history. It can also help those with poor or limited credit problems.

Learn More About Factors That Affect Credit Score

- What’s the Most Important Factor of Your Credit Score? The most important factor of your FICO Score is your payment history, which makes up 35% of your score. Here’s what other factors matter.

- What is a Credit Utilization Rate: Your credit utilization rate is the amount of revolving credit you’re currently using divided by the total amount of revolving credit you have…

- How to Improve Your Payment History: Maintaining a clean payment history—or refurbishing a spotty one—can help you improve your credit scores and save you money.

- How Does Length of Credit History Affect Your Credit?

The length of your credit history can directly impact your credit scores, and this scoring factor is often misunderstood.

Read Also:

- What Does Capital One Report to Credit Bureaus About Credit Score

- Repo: How Long Does a Repossession Affect Your Credit Score?

- Can you get Closed Account Removed from Credit Report?

- How can Poor Credit Score Hurt your Social Security Benefits?

What it is and How to Access it")