Removing a paid or unpaid repossession report from your credit report is not easy. Facing the need to search for “How to get a repo off your credit report” may not be a desirable situation for anyone. Life is unpredictable, and unforeseen circumstances can arise. Discovering that your vehicle is being repossessed due to defaulting on your auto loan can be incredibly distressing, especially when you witness your car being towed away, realizing it’s not a mere parking mistake.

Unfortunately, the situation tends to worsen as a defaulted auto loan is reported to consumer credit bureaus, resulting in its presence on your credit reports for a period of up to seven years. This negative mark can have significant implications for your creditworthiness and financial reputation.

Certainly, a negative mark from a defaulted auto loan can have a significant impact on your credit score, potentially causing difficulties in obtaining new credit and resulting in higher interest rates if you are approved.

While credit repair may offer an avenue for early removal of the negative mark, it is more likely that you will need to explore other credit-building solutions while waiting for the default to age off your credit reports. In this article, we will delve into the available options, including the possibility of early removal, the waiting period, and also explore second-chance auto loan options.

Can Credit Repair Helps to Remove a Repossession?

Credit repair services have the potential to remove a repossession from your credit report before the standard time period. By engaging in credit repair, you may have the opportunity to expedite the removal of the repossession entry, thereby improving your credit profile sooner than expected.

Once a repossession is reported to the credit bureaus, it is likely that your creditor has already repossessed the vehicle and potentially sold it. Consequently, the opportunity to negotiate with the creditor for removal of the negative mark from your credit reports becomes limited. At this stage, there are typically few options available to have the creditor remove the repossession entry from your credit history.

In such situations, credit repair emerges as the primary option to potentially remove the repossession from your credit report before its expiration date. While credit repair cannot guarantee results, it provides a possibility to dispute and potentially remove an inaccurate or unverified repossession mark from your credit report.

While you can file a credit report dispute on your own, enlisting the assistance of an experienced credit repair company may enhance the likelihood of success in the process.

Related Repo: How Long Does a Repossession Affect Your Credit Score?

Lexington Law

- Most results of any credit repair law firm

- Clients saw more than 7 million negative items removed from their credit reports in 2020

- More than 221 million challenges and disputes sent for clients since 2004

- Get started today with a free online credit report consultation

- Cancel anytime

| Better Business Bureau | In Business Since | Monthly Cost | Reputation Score |

|---|---|---|---|

| See BBB Listing | 2004 | $59.95+ | 8/10 |

Sky Blue Credit Repair®

- Best-in-class support

- In business since 1989

- Rapid 35-day dispute cycle, tailored to your situation

- 90-day 100% money-back guarantee

- Low $79 cost to get started, cancel or pause membership anytime

| Better Business Bureau | In Business Since | Monthly Cost | Reputation Score |

|---|---|---|---|

| A+ | 1989 | $79 | 9.5/10 |

Helpful Guides

- Credit Score Check, Reports and Highest Range in Your Finance

- Best Strategies to Improve Your Credit Score from 500 to 800

- How Can Poor Credit Score Hurt My Social Security Benefits?

- Can you get Closed Account Removed from Credit Report?

- Can I Get a Car Loan with a Repossession on my Credit?

CreditRepair.com

- Free online consultation

- Helped with over 8.2 million removals on members’ behalf since 2012

- Free access to your credit report summary

- Three-step plan for checking, challenging and changing your credit report

- Online tools to help clients track results

| Better Business Bureau Better Business Bureau | In Business Since | Monthly Cost | Reputation Score |

|---|---|---|---|

| See BBB Listing | 2012 | $69.95+ | 8/10 |

Understanding the limitations and scope of credit repair is crucial for achieving success. It is important to recognize that the Fair Credit Reporting Act (FCRA) grants you certain rights, including the right to fair and accurate credit reports. Consequently, you have the ability to dispute credit report items that are fraudulent, inaccurate, outdated, or unsubstantiated.

Knowing your credit scores can help you gauge the likelihood of your loan application getting approve and whether the creditor will offer you favorable terms. In other words, if the creditor is unable to provide evidence that the debt belongs to you, you have the right to challenge and potentially have such items removed from your credit report through the credit repair process.

Filing a Credit Report Dispute

Upon filing a credit report dispute, the credit bureau is obligated to initiate an investigation within 30 days. As part of this process, they will typically reach out to the party responsible for providing the disputed information, which, in the case of a repossession, would be the auto loan lender in most instances. The purpose of contacting the lender is to gather relevant details and evidence regarding the repossession, which will aid in assessing the accuracy of the reported information.

In the event that the lender is unable to provide sufficient evidence demonstrating your responsibility for the loan and the accuracy of the reported default, the credit bureau will proceed to remove the account from your credit reports.

However, if the lender is able to substantiate that the default was accurately reported, the credit bureau is not obligated to remove the account, and therefore it will remain on your credit reports. The decision to remove or retain the account ultimately depends on the strength of the evidence provided by the lender during the credit bureau’s investigation.

Wait 7 to 10 Until the Repo Ages Off Your Report

Car Repossession Stays 7 Years on Your Credit Report – When credit repair is not a viable option or has been unsuccessful in removing the negative item, the best course of action is to exercise patience and wait. Most negative credit report items, such as defaults and repossessions, typically have a natural expiration period of seven years, after which they should be automatically removed from your credit report.

It’s important to note that certain bankruptcies may remain on your credit reports for up to 10 years. During this waiting period, focus on practicing good credit habits and building a positive credit history to offset the impact of the negative item as it ages off your credit report.

Indeed, while a repossession may remain on your credit reports for up to seven years, its negative impact on your credit score diminishes over time. Credit scoring models often prioritize more recent information on your credit report, assigning it greater significance in determining your credit score. As the repossession ages, its influence on your credit score gradually diminishes.

Similar Financing Guides

- How to Choose the Best Bank to Open Checking Account

- 3 Ways American President Could Impact Social Security in the US

- What are the Best Steps to Lower Your Credit Card Interest Rate?

- Top 5 Impact of Artificial Intelligence on CyberSecurity

This means that as time passes, the negative impact of the repo will have less of an effect on your overall credit score calculation. It highlights the importance of focusing on positive credit behavior and diligently managing your credit going forward to mitigate the impact of past negative events on your creditworthiness.

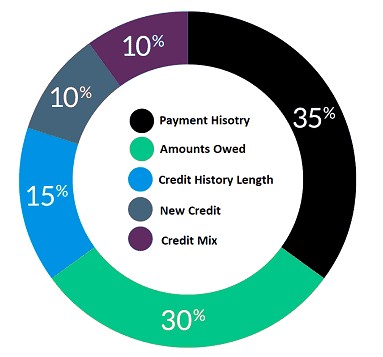

To mitigate the negative effects of a repossession on your credit, it is crucial to focus on improving the overall health of your credit profile. Defaulted loans and subsequent repossessions are categorized under the payment history section of your FICO credit score. Payment history carries a significant weight of 35% in determining your credit score.

Trust me, by prioritizing positive payment history and ensuring timely payments on your other credit obligations, you can offset the impact of the repossession on this factor. Building a strong and consistent payment history demonstrates responsible credit behavior and can help minimize the adverse influence of the repossession on your credit score.

Strategies to Increase Credit Score

It is important to know the 5 Factors That Affect Your Credit Score in your FICO Score Report. On the other hand, while focusing on payment history, it is essential to address other key factors that contribute to your credit score. Simply by working on these aspects, you can create a more balanced credit profile. Here are some strategies to consider:

1. Credit Utilization:

It is advisable to maintain low credit card balances in relation to your credit limits. High credit utilization can have a detrimental effect on your credit score. Aim to keep your credit utilization below 30% and ideally lower.

By keeping your credit card balances in check, you can minimize the negative impact on your credit score and demonstrate responsible credit management. See the 5 Steps to Lower Your Credit Card Interest Rate here.

2. Total Debt:

To effectively reduce your overall debt, it is essential to establish a robust repayment plan. Create a structured strategy that allows you to make consistent and timely payments towards your existing debts.

By doing so, you can gradually decrease your total debt over time and improve your overall financial standing.

3. Credit History Length:

The length of your credit history holds significance in determining your creditworthiness. It is beneficial to maintain long-standing accounts to showcase a solid credit history. If you have a limited credit history, it is advisable to keep older accounts open, as they contribute to establishing a longer credit track record.

By demonstrating a consistent and responsible credit history over time, you can enhance your credit profile and improve your overall creditworthiness.

4. New Credit Accounts:

To maintain a healthy credit profile, it is important to limit the opening of unnecessary new credit accounts. Each new account application can result in a temporary decrease in your credit score. Therefore, it is advisable to apply for credit only when necessary and avoid excessive credit inquiries. Carefully consider your credit needs and apply for new credit accounts only when it aligns with your financial goals and requirements.

By being selective and mindful about new credit applications, you can minimize the potential negative impact on your credit score and maintain a stable credit profile.

5. Credit Mix:

Strive to achieve a diverse mix of credit types in your financial portfolio, including credit cards, installment loans, or a mortgage. This approach demonstrates your ability to effectively manage different types of credit and showcases responsible credit behavior.

Having a varied credit mix can positively impact your credit score and signal to lenders that you can handle different financial obligations. However, it’s important to note that diversifying your credit should be done responsibly and within your means. Only take on credit types that align with your financial goals and ensure that you can manage them effectively.

In the long run, if you focus on these areas, you can gradually improve your credit profile and mitigate the impact of a less-than-stellar payment history caused by a repossession. Remember that positive credit habits and responsible financial management are key to rebuilding your creditworthiness over time.

Second-Chance Auto Loans Can Help You Down the Line

Rebuilding your credit score after the impact of a repossession and defaulted auto loan requires dedication and persistence. However, during this credit score recovery period, obtaining a new auto loan can present challenges. Most major banks may be hesitant to take on the risk of a potential second default, leading them to require at least two years of clean payment history before considering your loan application.

This prerequisite ensures that you have demonstrated responsible credit behavior over a significant period before being eligible for a new auto loan. It’s important to be patient, focus on improving your credit, and establish a solid payment history to increase your chances of qualifying for an auto loan in the future.

If waiting for the default to age or improving your credit score sufficiently is not feasible, exploring second-chance auto financing may be necessary. Second-chance auto lenders specialize in providing financing options for subprime borrowers and typically have more flexible credit score requirements. Utilizing online lending networks can enhance your chances of finding a lender who is understanding of your situation.

These networks offer a range of options that can increase your likelihood of securing a loan from a lender willing to work with your circumstances. Remember to carefully review the terms and conditions of any loan offer to ensure it aligns with your financial goals and repayment capabilities.

Auto Credit Express

- Network of dealer partners has closed $1 billion in bad credit auto loans

- Specializes in bad credit, no credit, bankruptcy and repossession

- In business since 1999

- Easy, 30-second pre-qualification form

- Bad credit applicants must have $1500/month income to qualify

| Interest Rate | In Business Since | Application Length | Reputation Score |

|---|---|---|---|

| 3.99% – 29.99% | 1999 | 3 minutes | 9.5/10 |

PenFed Credit Union

- Auto loan amounts of up to $150,000

- Prequalify in minutes without impacting your credit score

- Refinancing loans save an average of $191 per month

- 125% financing available for cash-out refis

- PenFed Credit Union membership required but can be applied for at the same time as your loan

| Interest Rate | In Business Since | Application Length | Reputation Score |

|---|---|---|---|

| 5.19% and up | 1935 | 5 minutes | 9.5/10 |

RefiJet

- RefiJet helps people lower their monthly auto payment by an average of $150 a month*

- Pre-qualifying for a refinance auto loan does not impact your credit score

- Nationwide network of lenders

- We present you with options from lenders that fit your situation

| Interest Rate | In Business Since | Application Length | Reputation Score |

|---|---|---|---|

| Varies | 2016 | 5 minutes | 9.0/10 |

While second-chance auto loans are available, it’s important to note that even subprime lenders may require a waiting period of several months after a repossession before considering your loan application. Additionally, you will need to meet the specific income requirements set by the lender. These income requirements typically start at a minimum of $1,000 per month, though they can vary and sometimes be higher.

It’s essential to research and evaluate the specific eligibility criteria of different lenders to determine which options may be suitable for your financial situation. By meeting the income requirements and waiting for the necessary duration post-repossession, you can increase your chances of securing a second-chance auto loan.

In general, it is often advisable to wait for a few years after a default before seeking another auto loan. This waiting period is beneficial because subprime auto loans typically carry high interest rates and may include additional fees, making them considerably more expensive in the long run compared to loans available to individuals with better credit.

By allowing time to improve your credit and financial situation, you can potentially qualify for loans with more favorable terms, lower interest rates, and fewer associated costs. Patience and focusing on rebuilding your credit can help you secure a more affordable auto loan in the future.

Good News: A Repossession Won’t Haunt You Forever

Experiencing the sight of your car being repossessed due to defaulting on your auto loan can be emotionally and financially distressing. The negative impact on your credit score can be long-lasting, making it challenging to obtain new credit. However, it’s important to remember that although a repossession may stay on your credit report for up to seven years, it is not a permanent setback. With time and effort, your credit can recover.

By taking steps to rebuild your credit, such as making consistent and timely payments, reducing debt, and maintaining a positive payment history, you can gradually improve your credit score. It’s crucial to be patient and persistent during this recovery process.

Over time, the negative effects of the repossession will diminish as positive credit behaviors take precedence. While the journey may take time, it’s important to remain optimistic and focused on rebuilding your credit for a brighter financial future.

Indeed, the best approach is to prevent your auto loan from defaulting in the first place. If you find yourself in a situation where you’re at risk of falling behind on your payments, it’s crucial to proactively reach out to your lender. Contacting your lender as soon as possible is essential because defaults are not beneficial for anyone involved. Lenders have a vested interest in helping you find a solution to repay your debt, but they can provide more assistance if you reach out to them before missing payments.

Helpful Credit Score Guideline:

- How to Prevent Fraud on Credit Card with Identity Theft Detection

- How to Consolidate Credit Card Debt without Hurting your Credit

- How to do Credit Card Balance Transfer to Another Issuer with No Fee

- Top 10 Credit Cards with No Annual Fee Debit or Service Charge

- Best Strategies to Improve Your Credit Score from 500 to 800

- Why does a Car Repossession Stays 7years on Your Credit Report

Conclusion

In summary, when you start communicating with your lender early, you can get better options such as loan modifications and refinancing. You can also create a revised repayment plan that aligns with your current financial situation.

Open and transparent communication can lead to finding mutually beneficial solutions that help you avoid defaulting on your auto loan and maintain a positive relationship with your lender.

There’s a guide on “How to Negotiate Debt Settlement with your Credit Card Company” to help you. Remember, taking proactive steps and seeking assistance promptly can significantly increase the chances of resolving financial difficulties and preventing the negative consequences of loan default.