Do you wonder what a FICO score is all about? It is the Fair Isaac Corporation score in the finance sector that shows if you are credit worthy. This article provides answers to your quest to as what a FICO score is all about and the range.

The FICO score is a credit scoring model develop by Fair Isaac corporation(FICO) considers different factors, such as payment history, outstanding debts, length of credit history, credit mix, and recent credit applications. These factors are used to calculate an individual’s credit score, which lenders use to assess the risk of granting credit to that person.

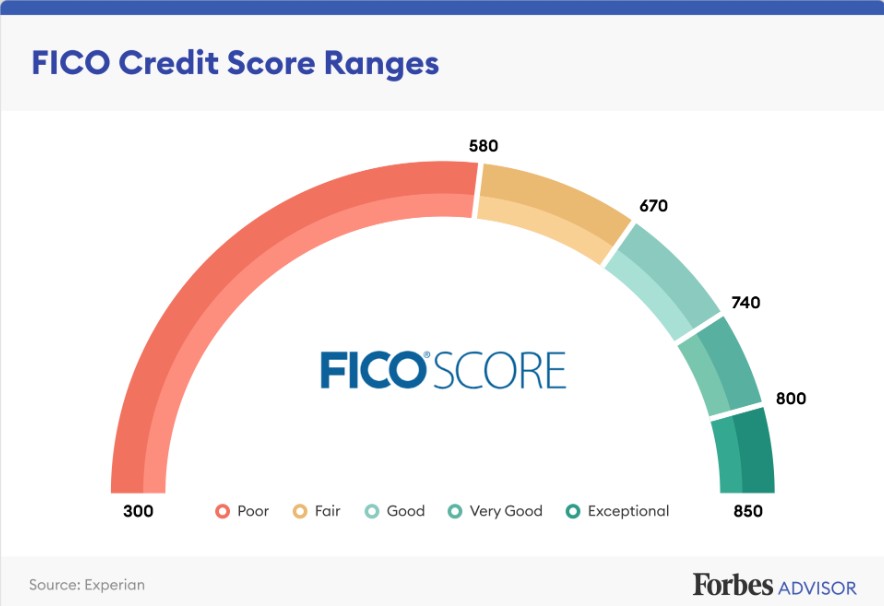

It is one of the most widely used credit scoring systems in the United States and is used by lenders to assess an individual’s creditworthiness. FICO scores range from 300 to 850, with higher scores indicating better creditworthiness.

A FICO score is a three-digit number ranging from 300 to 850 (and up to 900 for some industry-specific scores). These scores are largely based on your credit reports (statements generated by the consumer credit reporting bureaus that detail your credit activity and current credit situation) and can help creditors assess how likely you are to repay debt.

What is FICO Score all About and Its Importance?

FICO scores are widely used by different types of creditors, including lenders, credit card issuers, and insurance providers. They use these scores to assess your credit risk, which refers to how likely you are to repay the money you borrow.

Having higher credit scores increases your chances of securing loans with better rates and terms. On the other hand, lower scores may result in less favorable credit terms if you get approved at all.

For insurance companies, lower scores can lead to higher premium rates.

Knowing your credit scores can help you gauge the likelihood of your loan application getting approve and whether the creditor will offer you favorable terms. Some lenders may have specific score thresholds that applicants must meet to be approved.

You can check the lender’s website or ask a representative to find out if there are specific score requirements and which scoring models the company uses. However, some companies may not disclose this information.

Helpful Guides

- Credit Score Check, Reports and Highest Range in Your Finance

- Best Strategies to Improve Your Credit Score from 500 to 800

- How Can Poor Credit Score Hurt My Social Security Benefits?

- Can you get Closed Account Removed from Credit Report?

- Can I Get a Car Loan with a Repossession on my Credit?

What’s a good credit score

The answer depends on the lender or creditor that’s reviewing your scores and their criteria, but it’s important to know what range your credit scores are in. Higher credit scores are better than lower scores, and on the 300 to 850 scale, scores of 670 and above is consider “good.”

Why are there different FICO® scores?

There are dozens of different FICO scores, under two general categories.

- Base FICO scores (the most widely used type)

- Industry-specific FICO scores (tailored to certain credit products, such as credit cards or auto loans)

Periodically, FICO releases new versions of its credit scoring models with the aim of improving upon previous versions and providing lenders with more accurate and reliable scores.

This means that there can be multiple editions of each scoring model, but lenders have the option to continue using older versions if they prefer.

FICO has also developed three versions of its base FICO scores to align with data from the major consumer credit bureaus: Equifax, Experian, and TransUnion. The most recent edition is FICO Score 9, although some lenders may still rely on FICO Score 8 or an earlier version.

Also to the base scores, there are industry-specific scores like the FICO Bankcard Score and FICO Auto Score, which also have multiple versions and editions.

While it may be possible to contact a creditor and inquire about the specific credit-scoring model they use for evaluating applicants, the good news is that the key scoring criteria are generally similar across most FICO credit scores. Therefore, if one of your FICO scores falls within the “very good” range, it’s likely that your other FICO scores will also be in that range.

What Factors Affect FICO scores?

FICO credit scores depend on the information in your consumer credit reports, and different pieces of information may raise or lower your scores. For example, making on-time payments may help your scores, while a late payment could hurt it.

FICO breaks its scoring criteria down into five categories, with a percentage value based on each category’s importance, though the importance may vary for individuals.

1. Payment history (35%):

This is the most important factor in determining your credit scores. It looks at how well you’ve paid your bills on time and any negative records like bankruptcy.

2. Amounts owed (30%):

This factor considers how much you owe on your credit accounts, such as loans and credit cards, as well as the percentage of your available credit that you’re using (credit utilization rate).

3. Length of credit history (15%):

The age of your accounts, including the oldest and newest, and the average age of all your accounts contribute to this factor. It also takes into account the time since you last used certain accounts.

4. Credit mix (10%):

While not as important, having different types of accounts like credit cards, mortgages, and retail loans can have a positive impact on your scores.

5. New credit (10%):

This factor considers recent credit inquiries and newly opened accounts. It can affect around 10% of your scores.

While the exact percentage values differ depending on your overall credit file and the scoring model, understanding the relative importance of credit-scoring factors and what you can do to build good credit may help you improve your credit scores.

What’s next

Creditors can use FICO® credit scores to evaluate prospective customers and manage existing customers. Lastly, having an understanding of what affects your FICO credit scores could help you build good credit. This will in turn may help you get the best rates and terms on a future loan or credit card.

Read Also:

- What are the 5 Factors That Affect Your Credit Score? FICO Score Reports

- When Does Capital One Report to Credit Bureaus About Your Credit Score

- Cash Back Credit Cards: Types, Comparison, Rewards, Pros and Cons

What it is and How to Access it")