This guide will show you How to Complete Credit Card Balance Transfer from one Card to Another. After reading this article, it is sure that you will know how to do your balance transfer successfully. And you can do this transfer on any credit card of your choice without any hinderances. Choosing to transfer your balance to a lower-rate credit card usually assist people in paying off your debt more effectively. Normally, credit card companies generally charge a specific fee to transfer a balance. It is oftentimes about 3-5% of the total amount moved.

A credit card balance transfer can help you reach your goal in diverse ways. You can benefit from it whether you’re aggressively tackling your credit card debt or simply want to save a few cash on your monthly bill.

However, there are different strokes for different folks. That is; a balance transfer isn’t the best option for everyone. But, if you decide it’s the right move for you, then read on. I will still give you an idea of how it works and how to perform/complete a Credit Card Balance Transfers from one Card to Another.

How a Balance Transfer Works

In simple terms, a credit card balance transfer is simply when you move your credit card debt from one [credit card] to another company. Mrs. Tia Sabawi, the vice president of consumer lending at Xceed Financial Credit Union explains in an interview that you can transfer as much debt as your new card’s credit limit.

However, a balance transfers in general terms can’t be done in the same cards from one issuer but can be made using one issuer to another company. “On the long run, the main goal is to take repayment advantage of a lower interest rate”, says Sabawi. To be more specific, credit card companies will often offer an introductory 0% annual percentage rate on balance transfers for new customers. In fact, this is a strategy by the issuers to attract new business. Usually, this zero interest rate can last from twelve to twenty-one months. It is normal.

Now, if you currently have a balance on a high-interest credit card, you can simply transfer the balance to a new card with a lower rate. To be sincere, this can help you not only pay less interest but also pay off the balance faster and easily.

Example of How a Balance Transfer Works

In most cases, these credit card companies will charge a service fee to transfer a balance. The amount is usually about 3-5% of the total figure you transferred. Therefore, if you transfer a credit balance of $2,000, for example, expect to pay just $60 to $100 in fees.

“Bear in mind that each issuer will have different fees and terms for their balance transfers,” says Tai. Please note that it is very important to compare your upfront costs with the long-term interest savings. Why? So you can be sure a transfer of credit balance is worth it or not. For a softer landing, “There are some issuers that will offer a zero-dollar fee for your first transfer. While others may not charge you for transfers made in the promotional period,” she says.

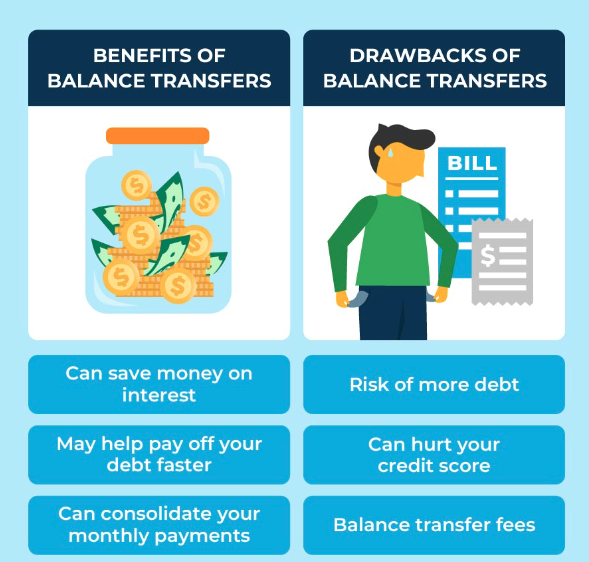

Credit Balance Transfer Pros and Cons

Lets take a look at the advantages and disadvantages of balance transfer. Even though it might be suitable to transfer you credit from one account to another you have to note this. When it comes to credit card balance transfers, there are a few undeniable benefits to customers. But those benefits don’t always outweigh the drawbacks. Thats the blunt truth. So, you’ll have to do the math yourself to make a decision if a balance transfer is worth it or not.

Special Benefits of Transferring a Credit Balance

These are the advantages you will get from an issuer if you successfully transfer your credit balance from one card to another.

- You can Save money: First of all, the main reason to transfer a balance is to simply save money on interest. This will definitely give you more monthly cash flow as well as avail you the opportunity to pay off your debt efficiently. In fact, by transferring your current debt to a single low-interest card, you’ll position yourself to make a single [smaller] payment each month. This will give you more opportunity to cut down on your credit debt. “It will help you to enjoy a little more breathing room each month,” says Tai Sabawi. Going by this, if you’re thinking of doing a credit balance transfer, it’s also a great time to reassess your budget. Just ensure you look for easier ways to keep yourself out from incurring future debt.

- It can Improve your credit score: Over the years, one positive advantage of paying down your credit card debt is that it will increase in your credit score. Note that your credit utilization makes up 30% of your credit score. Going by the books, experts advises people to keep their balance low (under 30% of your credit limit).

For more explanation, Tai Sabawi has this to says; “Transfer your debt if it is worth it and quick about it.” She continues; While a balance transfer is a good tool for improving your financial position and could net you a higher credit score, it’s important not to make a habit of transferring your debt.” This is simply because balance transfers could become a problem that eventually lands you back in debt if not used responsibly. Now lets take about the disadvantages of balance transfer.

Drawbacks of a balance transfer?

Why think twice about a balance transfer? We will explain two reasons.

- You may Incur transfer charges / fees: A balance transfer may or may not actually save you money. However, this depends on the difference between your old and new interest rate. Invariably, the only way we think it’s worth it is if the interest savings is better than the transfer fee. Also, ensure you apply for credit cards issuer that don’t charge a balance transfer fee. This is to make sure it’s a financially smart move.

- You can Potentially end up in more debt: Talking from experience, taking advantage of a balance transfer requires serious discipline. Take it or leave it. For instance, if instead of paying off your balance faster, you use your “savings” to spend more, all the benefits are clearly lost. Reason it for one minute, you will see its true. Therefore, you should run the numbers to confirm you’ll be able to pay off the debt based on the terms. If not, you might end up back where you began from.

Below are other similar posts to guide you further.

- 5 Steps to Lower Your Credit Card Interest Rate

- Credit Score Check, Reports and Highest Range in Your Finance

- How to Negotiate Debt Settlement with your Credit Card Company

- How to Borrow Money with Instant Cash Advance from your Credit Card

- Paying Back-to-School Expenses with No Money – Help to Pay Tuition

- Find Your Dream Job Here to Launch Your Career – Future starts today

How to Transfer a Balance from one Issuer to Another

How to do Credit Card Balance Transfers: Now, if a person decides that a credit balance transfer will assist him/her to reach their financial goals, then continue reading. The reason is because it is fairly simple to accomplish. Below are the simple steps to take to transfer your credit balance from one card issuer to another.

1. Review your credit score.

Is your credit score in good shape? As a debtor, the first thing you have to do before actually submitting a balance transfer request is to ensure your credit score is in one piece. “Please, don’t ever make the mistake of trying to transfer your balance when you have poor credit,” warns Rachel Smith Natasha. (She’s the global head of communications and public relations, and consumer affairs expert at rebate website TopCashback). A good credit is not only needed to qualify for a card in most cases, but “the best terms are only available to those with a good or excellent track record,” she adds.

2. Research the Best interest rate offers.

As can be seen above, we have said that interest rates and fees vary across different issuers and cards. Therefore, it’s very crucial to search widely and discover the best deal for your credit profile. All these also includes the lowest fees, the lowest rate, and in the case of zero percent Annual Percentage Rate (APR) offers, the longest promotional period. These are the Best Low Interest Rate Credit Cards for 6 to 24 months you can see in the US.

“The longer you have to repay at this cheaper rate, the more manageable and achievable it will feel to reach the goal of a zero-dollar balance,” says Smith.

3. Calculate the numbers.

Calculation of interest rate is very important. So, ensure that the cost of transferring a balance doesn’t outweigh the debt making the interest savings useless. Also, be on the lookout and note that “the fee is determined by the bank. It is as well typically based on how much money you’d like to transfer,” says Smith. In black and white explanation; the bigger your balance, the bigger the fee you will pay.

4. Submit an Application to Sign Up an Account.

After you’ve successfully chosen the best credit card suitable for you, it’s now time to submit an application to open an account and transfer a balance. This can be done online through the card issuer’s website or via the bank’s customer service phone number. These are the Best Bonus Credit Cards to Sign-up for as a New or Existing Bank Account Holder.

All together, you’ll be needing your account information as a prerequisite for the balance you are transferring. In addition, you should have the card number handy together with exact amount you want to transfer. Lastly, you’ll also need to make provision for your personal details, including your address, monthly income and Social Security number (SSN). Please make sure you are using the official bank website. Don’t fall into a fake website to prevent scam. These are the Best Ways to Prevent Fraud on Credit Card with Identity Theft Detection.

5. Ensure You Double Check Everything is ready.

Immediately you get approval, the new credit card issuer will swiftly facilitate the balance transfer. In fact, this usually takes about 7 to 10 days. However, please note that; until the transfer is completed, you still owe that amount on your old card and are responsible for interest charges and payments.

But once the transfer is successful, its important that you do a smooth follow up to ensure the correct amount was transferred as requested. Furthermore, if you’re having the though of closing your old card account, you have to give it a proper consideration. “Even though it is tempting to close the card you just completely made payment for, canceling could reduce/damage your credit score.” says Smith. Reason is simply because you will lower the total amount of credit available to you. While on the other hand increasing your credit utilization – immediately.

Another important fact to note; if you keep your old card open after transferring out your credit, ensure that no extra charges, interest fees or recurring payments were charged after the balance transfer took place. Best bet is to set up account notification alerts to keep tabs on any activity.

6. Set up automatic payments.

The last part is setting yourself up for success by paying down your balance every month. is is also best if you keep avoiding new debt. As far as no new transaction happens in that account, it can help know what you owe. Therefore, setting up automatic payments from your checking account will always remind you so you don’t forget.

“Lastly, old habits are hard to crack off, especially when it comes to spending money,” says Smith. But after going through these 6 steps above to successfully transfer your credit card balance, you must definitely want it to be worth the while. “I advise you to seriously focus on paying the old debt on time every month and eliminating your credit balance,” she says. This article; Paying Back-to-School Expenses with No Money – Help to Pay Tuition Bills explains more. There are other similar guides to help you push through.