A mortgage calculator is a tool that helps you estimate how much your monthly mortgage payments would be based on certain inputs. All you have to do is to enter your details such as the loan amount, interest rate, and loan term, the calculator can calculate an estimate of your monthly payments.

The mortgage calculator can be useful for understanding how different factors, such as loan amount or interest rate, can affect your monthly budget when you’re considering a mortgage. If you want to know how much is Mortgage Payments, then Calculate using Interest rate, Taxes and Insurance [Online Calculator].

Take the next step with a pre-approval

It takes as little as 3 minutes. A customizable pre-approval letter helps you make a personal offer quickly. Get pre-approved

How to calculate mortgage payments

Your monthly mortgage expenses go beyond just loan payments and interest. To help you calculate all the costs involved in owning a home, we’ve included various typical monthly expenses.

You can experiment with different home prices, locations, down payments, interest rates, and mortgage lengths to understand how they impact your monthly mortgage payments.

If your down payment is less than 20% of the home price, private mortgage insurance (PMI) costs will be added to your monthly payment. We’ve also provided an estimate for utilities, which can vary by county and can be broken down by service. If you’re considering a condo or a community with a Homeowners Association (HOA), you can include HOA fees in your calculations.

Please note that we haven’t included the costs of annual home maintenance/repairs or home improvements. To determine how much home you can afford, including these costs, you can use the Better home mortgage calculator.

Interesting fact

Property tax rates are highly localized, meaning neighboring homes of similar size and quality could have different tax rates due to municipal borders. Buying a home in an area with lower property tax rates may make it more feasible to afford a higher-priced home.

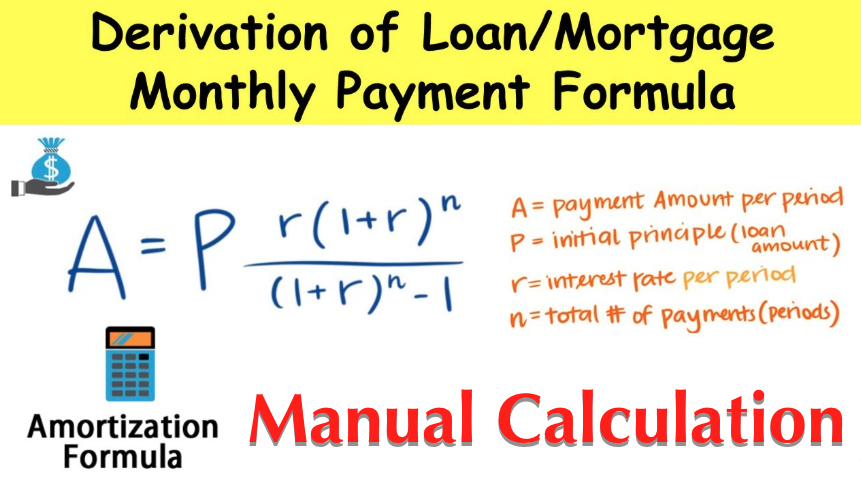

Mortgage Calculator Formula

Ways this free mortgage calculator is different

This mortgage calculator shows your payments with taxes and insurance

As a homeowner, you have the responsibility of paying property taxes and homeowners insurance. These costs also include in your mortgage payments to ensure they are kept up to date and protect your investment, which is important for both you and your lender.

Property taxes contribute to funding various community services provided by the local government, such as schools, libraries, roads, parks, water treatment, police, and fire departments. Even after you’ve paid off your mortgage, you will still be required to pay property taxes. Falling behind on property taxes could result in the risk of losing your home to the local tax authority.

During the mortgage repayment period, your lender will typically require you to have homeowners insurance. This is because lenders understand the importance of protecting the property from damage or destruction, such as fire, accidents, or natural disasters.

Interesting fact

Once you fully own your home, the decision to maintain homeowners insurance is up to you. However, to ensure coverage for potential damages cause by fires, lightning strikes, and natural disasters that can impact your area, it is generally recommend to keep homeowners insurance in place.

This mortgage calculator shows your mortgage costs with PMI

Private Mortgage Insurance (PMI) is a type of insurance that allows homebuyers to qualify for a mortgage with a smaller down payment, typically less than 20%. By opting for a mortgage with PMI, you can purchase a home sooner and start building equity while keeping cash in your savings account for other needs.

Many homebuyers choose mortgages with PMI. In fact, in July 2021, 71% of first-time homebuyers had a down payment of less than 20%. The median down payment for first-time homebuyers in 2020 was just 7%, and it has remained below 10% since 1989.

With conventional mortgages, PMI is automatically remove once the equity in your home reaches 22%. Alternatively, if you have earned at least 20% home equity, you can request the removal of PMI. This allows you to potentially save on insurance costs as you build equity in your home over time.

This mortgage calculator includes HOA fees

Homeowners association fees are typically charge directly by a homeowners association, but as HOA fees come part and parcel with condos, townhomes, and planned housing developments, they’re an essential factor to consider when calculating your mortgage costs.

Homes that share structural elements, like roofs and walls or community elements such as landscaping, pools, or BBQs, typically require homeowners to pay HOA fees to maintain the upkeep of these amenities.

While you’re still in your budget planning stage, it’s good to remember that HOA fees typically increase annually. HOAs may also charge additional fees known as ‘special assessments’ to cover unexpected expenses from time to time.

Useful Guides

- Advantages and Disadvantages of Joint Mortgage Loan for Family Home

- How Much does Mortgage Loan Officer Earns as Salary or Commission?

- What Happens When Lenders Repossess Homes on Mortgage?

- How Much for Pet Insurance Care and What does it Cover?

How to reduce your monthly mortgage payments

If you are unable to negotiate a lower purchase price with the seller, there are still alternative options available to you. Here are a few options to consider:

Extend the length of your mortgage

Choosing a longer loan term, such as a 30-year fixed rate mortgage, can result in lower monthly mortgage payments. When you extend the length of your mortgage, you have more time to pay off the loan, which spreads the payments over a longer period.

By opting for a 30-year term instead of a shorter term like 15 or 20 years, you can have more manageable monthly payments. This can be beneficial for individuals who want to prioritize affordability and have more flexibility in their monthly budget.

Increase your down payment

Making a larger down payment when buying a home can lead to smaller monthly mortgage payments. If you can put at least 20% of the home’s price as a down payment, you can avoid private mortgage insurance (PMI), which adds to your monthly costs.

Even if you can’t reach the full 20% down payment, increasing your down payment can still be beneficial. A higher down payment will help you get rid of PMI sooner, reducing your monthly expenses. For example, boosting your down payment by 5% can lead to lower monthly PMI fees, saving you money in the long run. So, putting more money down upfront can have a positive impact on your monthly budget and overall homeownership costs.

Get a lower interest rate

Increasing your down payment can help you qualify for a lower interest rate. The ratio of your down payment to the loan amount is call the loan-to-value ratio (LTV). A lower LTV can increase the likelihood of getting a low interest rate.

If you plan to stay in your home for a long time, you can consider buying points to lower your interest rate. Buying points means paying more upfront but getting a lower monthly payment.

If you expect to sell or refinance your home within the first 5-10 years of the mortgage, you can consider an adjustable-rate mortgage (ARM). An ARM offers a low fixed interest rate for an initial period (usually 5, 7, or 10 years).

After that, the interest rate can adjust, either going up or down. The initial interest rate for ARMs is typically lower than that of a conventional fixed-rate mortgage, making it a good option if you won’t keep the mortgage for long.

If you’re not planning to buy a home soon, improving your credit score can increase your chances of qualifying for a lower interest rate. By reducing your debt-to-income ratio (DTI), lenders will see that you can comfortably afford your mortgage and may offer a lower interest rate.

Next steps to buying a house

There are 8 steps to buying a house, and using this calculator helps you complete steps 1 and 2. The next step is getting pre-approval for a mortgage, which you can do quickly and easily with Better Mortgage.

It’s a free and no-commitment process that doesn’t affect your credit score. Getting pre-approval allows you to know how much home you can afford, the mortgage options available to you, and the range of interest rates you may be offered.

If you’re ready to buy a home now, continue reading from this website because my definitive home buying checklist can guide you through the process. With a pre-approval letter from Better Mortgage, you’ll have proof of your financial readiness to purchase, giving you an advantage over other buyers.

Plus, if you work with Better Real Estate and fund with Better Mortgage, you can save $2,000 on closing costs and potentially save up to $8,200 on average over the life of your loan.

Note that this article is for information purpose only.

Read Also:

- Mortgage Payment Calculator – How to Calculate Your Loan Payments for Free

- 10 Important Mortgage Terminology About Home Loan Financing and Banking Terms

- Joint Mortgages Loan: How to Buy a Home with Family Member [Husband, Wife, Children

- Top Mortgage Lenders for Low Interest Rate and No Down Payments for First Time.

![9 Best Retirement Plans for Salary Jobs and Business Owners [Explained]](https://hybridcloudtech.com/wp-content/uploads/2023/03/9-Best-Retirement-Plans-for-Salary-Jobs-and-Business-Owners-Explained-100x70.png "9 Best Retirement Plans for Salary Jobs and Business Owners [Explained]")