Have you ever wondered how much a mortgage might cost you when buying a home and using a Mortgage Calculator to check you monthly payments? Well, I’ve got something cool to share with you – it’s called a mortgage calculator! It’s a simple tool that helps you estimate how much your monthly mortgage payments could be based on different factors like the loan amount, interest rate, and loan term.

With a free mortgage calculator, you can play around with different scenarios and see how changes in these factors affect your payments. It’s like having a system that lets you peek into the future of your finances!

Whether you’re planning to buy your first home or considering refinancing, this mortgage amortization calculator can give you a clearer picture of what to expect. No more guessing or complicated math – just input the numbers, hit the calculate button, and voila! You’ll get an estimate of your monthly payments.

So, the next time you’re curious about your mortgage options, give the mortgage calculator a try. You can try the Google’s mortgage calculator that shows you what you can expect to pay each month. There are also other free online mortgage calculator. However, I’m your friend that can help you make more informed decisions about your homeownership journey. Happy calculating as you join me while I give you a full explanation!

Financial Considerations of using mortgage calculator

When using a mortgage calculator, there are several financial considerations to keep in mind:

- Loan Amount: The calculator allows you to input the loan amount you plan to borrow. Consider your budget and financial situation to determine a suitable loan amount that you can comfortably afford to repay.

- Interest Rate: The interest rate plays a significant role in determining your monthly mortgage payments. It’s crucial to consider current interest rates and choose a competitive rate that aligns with your financial goals.

- Loan Term: The mortgage calculator lets you input the loan term, which is the duration over which you’ll repay the loan. Shorter loan terms generally have higher monthly payments but result in less overall interest paid, while longer terms have lower monthly payments but may accrue more interest over time. Consider your financial goals and choose a loan term that suits your needs.

- Down Payment: The calculator may allow you to input a down payment amount. A larger down payment can reduce the loan amount and potentially lower your monthly payments. Consider how much you can afford to put down and how it will impact your overall financial situation.

- Monthly Payments: The mortgage calculator provides an estimate of your monthly payments based on the loan amount, interest rate, and loan term. This helps you gauge whether the payments align with your budget and financial capabilities.

- Total Interest Paid: The calculator can also provide an estimate of the total interest paid over the life of the loan. This allows you to understand the long-term financial implications of your mortgage, helping you make informed decisions.

Other Financial Considerations

In addition to making your monthly payments, there are other financial considerations that you should keep in mind, particularly upfront costs and recommended income to safely afford your new home.

Recommended Minimum Savings

Let’s say we have $41,439 for example.

Recommended Minimum Income

$110,148 – Show Explanation

How Mortgage Calculator Get Answer

About Answers of Mortgage Amortization calculator

The calculator determines your monthly mortgage payment based on the inputs you provide, including home price, mortgage rate, loan term, and downpayment.

It calculates both the principal and interest portions of your monthly payments. Additionally, the calculator considers property taxes, mortgage insurance, and homeowners fees based on loan limits and location-specific figures. You have the option to manually adjust these fees in the tax insurance & HOA Fees section.

The calculator also shows how your mortgage balance changes over time as you make payments towards the principal and interest. Note that the figures do not include payments made towards taxes or other fees.

Do you have additional questions about this calculator? Feel free to check our previous guides for further understanding.

Assumptions of Answer from Mortgage Calculator

This calculator does not factor in home value appreciation or inflation when providing a comparison with your finances over a year. It focuses solely on determining monthly mortgage payments based on the inputs you provide.

How Your Mortgage Payment Is Calculated

Normally, mortgage calculator provides an estimation of your monthly mortgage payment, taking into account various components such as the loan’s principal, interest, taxes, homeowners insurance, and private mortgage insurance (PMI).

You have the flexibility to adjust parameters like the home price, down payment amount, and mortgage terms to observe how these adjustments impact your monthly payment amount.

If you’re not sure about the amount of money you should budget for a new home, you can also give our home affordability calculator a try. It can assist you in determining a suitable budget based on your financial situation.

Additionally, considering the complexities involved in purchasing a home, consulting with a financial advisor can be highly beneficial. To find a financial advisor who serves your area, you can utilize our free online matching tool, which helps connect you with suitable professionals. They can provide guidance and expertise to help you plan for the purchase of your dream home.

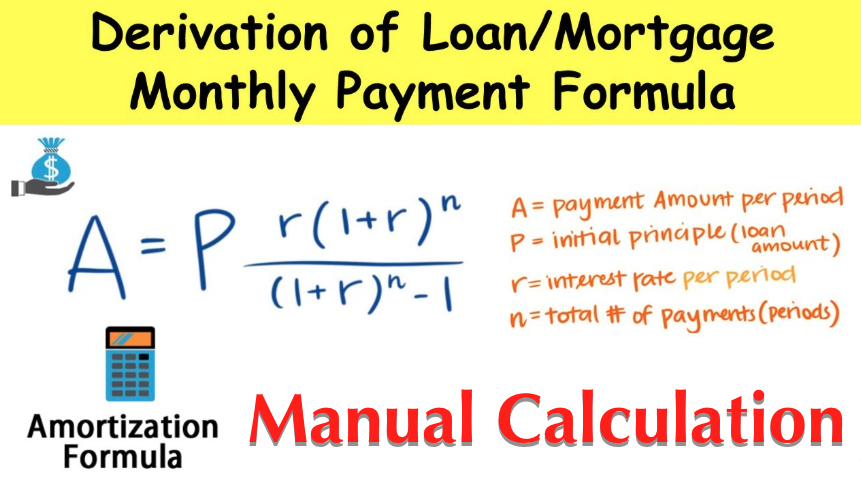

Mortgage Payment Formula

For those who want to know the math that goes into calculating a mortgage payment, we use the following formula to determine a monthly estimate:

M = Monthly Payment

P = Principal Amount (initial loan balance)

i = Interest Rate

n = Number of Monthly Payments for 30-Year Mortgage (30 * 12 = 360, etc.)

How SmartAsset’s Mortgage Payment Calculator Works

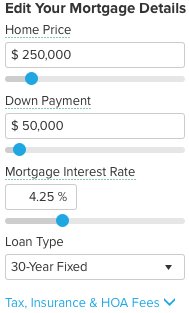

To determine your monthly payment, the first step is to provide some background information about your prospective home and mortgage. You’ll need to fill in three fields: home price, down payment, and mortgage interest rate. In the dropdown box, select your loan term. If you don’t have exact numbers, don’t worry – you can use your best guess. The numbers can be adjusted later if needed.

For a more comprehensive monthly payment calculation, you can click on the dropdown labeled “Taxes, Insurance & HOA Fees.” In this section, you can provide additional details such as the home location, annual property taxes, annual homeowners insurance, and monthly HOA or condo fees (if applicable). Simply by filling out this information, you’ll obtain a more accurate estimate of your monthly payment.

Factors That Determine Your Mortgage Payment

The mortgage payment calculator takes into account four important factors to estimate your monthly payment: home price, down payment, mortgage interest rate, and loan type. Let’s break down each factor and understand how it influences your payment:

1. Home Price

The home price, which is the first input for our calculator, is determined based on various factors including your income, monthly debt payments, credit score, and down payment savings.

As a homebuyer, you may come across the 28/36 rule or the debt-to-income (DTI) rule. According to this rule, your mortgage payment should not exceed 28% of your monthly pre-tax income, and your total debt payments should not exceed 36% of your income. This ratio helps lenders assess your financial capacity to make monthly mortgage payments. A higher ratio indicates a higher likelihood of struggling to afford the mortgage.

Here’s the formula for calculating your DTI:

DTI = Total Monthly Debt Payments ÷ Gross Monthly Income x 100

To calculate your Debt-to-Income (DTI) ratio, you need to follow these steps:

- Firstly, add up all your monthly debt payments. This includes payments for credit card debt, student loans, alimony or child support, auto loans, and the projected mortgage payment.

- Secondly, divide the total amount of your monthly debt payments by your monthly pre-tax income.

- Thirdly, multiply the result by 100 to convert it into a percentage.

The resulting number is your Debt-to-Income (DTI) ratio, which represents the percentage of your monthly income that goes towards paying off debt. This ratio is an important indicator for lenders to assess your financial capacity to handle additional debt, such as a mortgage. A lower DTI ratio generally indicates a healthier financial situation and a higher likelihood of being approved for a mortgage.

2. Down Payment

In general, most mortgage lenders prefer a 20% down payment for conventional loans to avoid the need for private mortgage insurance (PMI). However, there are exceptions to this rule.

For example, VA loans do not require any down payment, and FHA loans often allow down payments as low as 3%, although they do come with a form of mortgage insurance.

Furthermore, some lenders offer programs that allow down payments as low as 3% to 5%. The table below illustrates how the size of your down payment can impact your monthly mortgage payment.

[The table would provide a breakdown of different down payment percentages (e.g., 3%, 5%, 10%, 20%) and their corresponding effect on the monthly mortgage payment. It would demonstrate that a larger down payment typically leads to a lower monthly payment due to a reduced loan amount and potentially lower interest rates.]

How a Larger Down Payment Impacts Mortgage Payments

| Percentage | Down Payment | Home Price | Principal & Interest |

|---|---|---|---|

| 20% | $40,000 | $200,000 | $804 |

| 15% | $30,000 | $200,000 | $854 |

| 10% | $20,000 | $200,000 | $905 |

| 5% | $12,500 | $200,000 | $955 |

| 0% | $0 | $200,000 | $1,005 |

*The payment calculations above do not include property taxes, homeowners insurance and private mortgage insurance (PMI).

As a general guideline, it is advisable for most homebuyers to save up 20% of their desired home price before applying for a mortgage. Having a substantial down payment increases your chances of qualifying for the most favorable mortgage rates.

Your credit score and income are also significant factors that influence your mortgage rate, and subsequently, your payments over the long term. Hopefully, a higher credit score and a stable income can potentially lead to lower interest rates, reducing your overall mortgage costs.

1. Mortgage Rate

To determine your mortgage rate, you can utilize a mortgage rates comparison tool to see what you may qualify for. Alternatively, if you have already gone through the pre-approval process or spoken with a mortgage broker, you can use the interest rate provided by them.

In case you don’t have a specific rate in mind, you can estimate it by referring to the current rate trends on our website or your lender’s mortgage page. However, it’s important to remember that your actual mortgage rate will be based on various factors, including your credit score and debt-to-income ratio. These factors will be assessed by the lender to determine the most appropriate rate for your mortgage.

Helpful Guides

- Best Canadian Mortgage rates: Market Update- Factors and Terms

- Current Mortgage Rates Today to Compare Weekly Low Interest Rate

- Mortgage Loan Rates Today: Compare Rates Up-rise and Drops

- Home Mortgage Demand drops to Lowest Level as Interest Rate rises

- Mortgage Interest rates Drops When Exactly as Projected in 5 years?

- JPMorgan warns UK interest rates could hit 7% in Car and Mortgage Loan

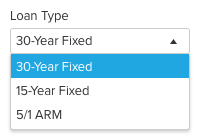

2. Loan Type

Within the drop-down area, you have the option to select from three types of mortgages: 30-year fixed-rate mortgage, 15-year fixed-rate mortgage, or 5/1 ARM.

The first two options, the 30-year and 15-year fixed-rate mortgages, are loans with a consistent interest rate and monthly payment throughout the entire loan term.

On the other hand, the 5/1 ARM, which stands for a 5-year adjustable rate mortgage, features an interest rate that remains fixed for an initial period and then adjusts annually. Following the introductory period, the interest rate can fluctuate based on prevailing market conditions. It can either increase or decrease, depending on the economic climate.

While the majority of people choose the stability of a 30-year fixed-rate loan, an ARM might be suitable if you plan to move in a few years or if you intend to sell the property relatively quickly. The ARM option could offer you a lower initial interest rate, potentially resulting in lower initial monthly payments.

3. Costs Included in Your Monthly Mortgage Payment

Here are two formulas to visualize the costs that are included in your monthly mortgage payment:

Monthly mortgage payment = Principal + Interest + Escrow Account Payment

Escrow account = Homeowners Insurance + Property Taxes + PMI (if applicable)

The monthly payment made to your mortgage lender consists of various components. For most homebuyers, an escrow account is established by the lender. This account is used to pay for property tax bills and homeowners insurance.

As a result, your monthly mortgage bill includes more than just the principal and interest payment (the amount that directly reduces your loan balance). It also incorporates homeowners insurance, property taxes, and, in certain situations, private mortgage insurance and homeowners association fees.

Let’s break down these costs:

- Principal and Interest: This portion of your payment goes towards repaying the principal amount borrowed and the interest charged by the lender.

- Homeowners Insurance: The cost of insuring your home against potential damages or losses is included in your monthly payment.

- Property Taxes: A portion of your payment is allocated to cover your property taxes, which are typically assessed by local government authorities based on the value of your property.

- Private Mortgage Insurance (PMI): If your down payment is less than 20% of the home’s purchase price, you may be required to pay PMI. This insurance protects the lender in case of default and is typically included in your monthly payment.

- Homeowners Association (HOA) Fees: If your property is part of a homeowners association, the fees associated with community maintenance and amenities may be included in your monthly payment.

Make sure you understand these cost breakdowns, so that you can have a clearer picture of how your monthly mortgage payment is allocated among various expenses.

4. Principal and Interest

The principal refers to the initial loan amount borrowed, while the interest is the additional amount owed to the lender over time, calculated as a percentage of the original loan.

In the case of fixed-rate mortgages, the total monthly payment for principal and interest remains the same throughout the loan term. However, the specific amounts allocated to principal and interest change as you make payments and gradually pay off the loan. This process is called amortization. Initially, a higher percentage of your payment goes towards interest, while over time, more of your payment is applied towards reducing the principal balance, resulting in less interest paid.

To illustrate this, let’s consider an example of a $200,000 mortgage. The table below demonstrates the breakdown of payments and how they contribute to the amortization process:

| Payment Number | Principal Payment | Interest Payment | Total Payment |

|---|---|---|---|

| 1 | $375 | $667 | $1,042 |

| 2 | $376 | $666 | $1,042 |

| 3 | $377 | $665 | $1,042 |

| … | … | … | … |

| 360 | $1,034 | $8 | $1,042 |

As you can see, with each payment, the amount applied towards the principal gradually increases, while the interest portion decreases. By the end of the loan term, the principal balance will be fully paid off. It’s as simple as that.

This example provides an overview of how amortization works and the changes in the principal and interest components over the life of a mortgage.

Helpful Guides

- Credit Score Check, Reports and Highest Range in Your Finance

- Best Strategies to Improve Your Credit Score from 500 to 800

- What are the 5 Factors That Affect Your Credit Score? FICO Score

- Who Can Override The Power of Attorney for Property?

- Power of Attorney (What is the Meaning, Forms, How to Get it)

- What is Mortgage Home Loan, Types and Process of Securing it?

Home Loan Amortization Table from Mortgage Calculator

| Payment Month | Principal | Interest | Total Payment |

|---|---|---|---|

| 1 | $303.90 | $616.67 | $920.57 |

| 60 (5 years in) | $364.43 | $556.14 | $920.57 |

| 120 (10 years in) | $438.37 | $482.20 | $920.57 |

| 180 (15 years in) | $527.30 | $393.27 | $920.57 |

| 240 (20 years in) | $634.28 | $286.29 | $920.57 |

| 300 (25 years in) | $762.96 | $157.61 | $920.57 |

*This table depicts loan amortization for a $200,000 fixed-rate, 30-year mortgage. The payment calculations above do not include property taxes, homeowners insurance and private mortgage insurance (PMI).

1. Homeowners Insurance

Homeowners insurance is a policy obtained from an insurance provider to safeguard against potential losses resulting from theft, fire, or damage caused by storms (such as hail, wind, and lightning) to your home. It’s important to note that flood or earthquake insurance typically requires a separate policy. The cost of homeowners insurance can vary significantly, ranging from a few hundred dollars to several thousand dollars, depending on factors like the size and location of your home.

When you borrow money to purchase a home, your lender typically mandates that you have homeowners insurance. This insurance coverage serves to protect the lender’s collateral, which is your home, in the event of fire or other damaging incidents. By requiring homeowners insurance, the lender aims to mitigate potential risks and ensure the protection of their investment.

2. Property Taxes

As a property owner, you are officially obligated to pay taxes imposed by the county and district authorities. You can use any property tax calculator by entering your zip code or town name to obtain the average effective tax rate in your area.

Property taxes can significantly differ from state to state and even within counties. For instance, New Jersey has the highest average effective property tax rate in the United States, standing at 2.42%. On the other hand, Wyoming boasts one of the lowest average effective tax rates at approximately 0.57%.

The calculation of property taxes generally involves a percentage of your home’s value and is typically billed on an annual basis. The frequency of reassessment varies depending on the state, county, and municipality. Some areas reassess property values annually, while others do so every five years. These taxes typically contribute to funding various services, including road repairs and maintenance, school district budgets, and general county services.

It’s important to note that property tax rates and the specific allocation of funds can vary significantly depending on your location. Using a property tax calculator can provide you with an estimate of the average effective tax rate applicable to your area.

3. PMI

Private mortgage insurance (PMI) is an insurance policy that lenders require for loans considered to be high risk. It is mandatory to pay PMI if you do not have a 20% down payment and do not qualify for a VA loan. The reason lenders typically require a 20% down payment is to establish equity. If you do not have sufficient equity in the home, you are seen as a potential liability for defaulting on the loan. Essentially, when you contribute less to the home’s value, you present more risk to the lender.

The cost of PMI is calculated as a percentage of your original loan amount and can range from 0.3% to 1.5%, depending on factors such as your down payment and credit score. Once you have reached at least 20% equity in the home, you have the option to request the discontinuation of PMI payments. This occurs because as you build equity, you become less of a risk to the lender.

It’s important to note that PMI serves to protect the lender in case of default and does not provide any direct benefit to the borrower. Once you have achieved a significant amount of equity, you can explore the possibility of eliminating the PMI requirement.

4. HOA Fees

When you want to buy a condominium or a home in a planned community, it is common to encounter homeowners association (HOA) fees. These fees are typically charged on a monthly or yearly basis. They are basically intended to cover common expenses related to the upkeep and maintenance of shared amenities and community spaces, such as the landscaping, community pool, or other communal facilities.

During your property search, HOA fees are usually disclosed upfront, allowing you to see the amount paid by current owners on a monthly or annual basis. It’s important to note that HOA fees are an ongoing additional expense to consider, separate from property taxes or homeowners insurance, in most cases. They contribute specifically to the costs associated with managing and maintaining the shared areas and facilities within the community.

When evaluating properties, it’s essential to factor in the HOA fees as part of your overall budget and financial planning, as they can significantly impact your monthly housing expenses. Understanding the specific details and coverage of the HOA fees is crucial to ensure you are fully aware of the financial obligations associated with the property you are considering.

New Related searches for Mortgage Calculator

- simple mortgage calculator

- google mortgage calculator

- mortgage repayment calculator

- simple mortgage calculator formula

- monthly payment calculator

- mortgage calculator zillow

- mortgage loan calculator

- mortgage payoff calculator

How to Lower Your Monthly Mortgage Payment

There are four common ways to lower your monthly mortgage payments:

- Choose a long loan term

- Buy a less expensive house

- Pay a larger down payment

- Find the lowest interest rate available to you

Normally, if you want to reduce your monthly mortgage payment, there are several strategies you can consider:

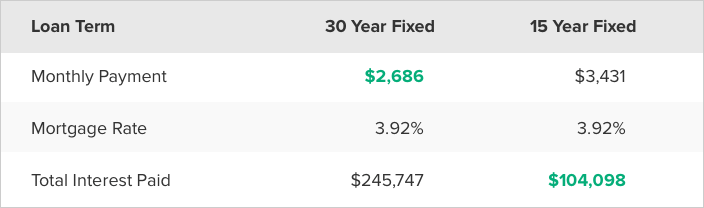

- Extending Loan Term: Increasing the number of years you’re paying the mortgage by opting for a longer loan term. This can result in smaller monthly payments. For example, a 30-year mortgage typically has lower monthly payments compared to a 15-year mortgage, as the loan is spread out over a longer period.

- Choosing a More Affordable Home: Purchasing a more affordable home can lead to lower monthly payments. The price of the home directly impacts your mortgage payment. So choosing a property within a lower price range can help reduce your monthly financial commitment.

- Managing Private Mortgage Insurance (PMI): If you are unable to make a 20% down payment, you may be required to pay for private mortgage insurance (PMI). To avoid this additional expense, consider buying a home at a lower price or waiting until you have saved a larger down payment.

- Seeking a Lower Interest Rate: Your interest rate significantly affects your monthly payments. Don’t settle for the first terms you receive from a lender. Shop around and compare offers from multiple lenders to secure a lower interest rate. Lastly, this can help keep your monthly mortgage payments as low as possible.

Truthfully, if you make use of these strategies, you can work towards reducing your monthly mortgage payments and improving your financial situation.

Editor’s Pick for More Information

All these guides is for Google Search mortgage tools: calculator, rates and definition of mortgage calculator. I hope this guide is helpful. If yes, please share. Lastly, feel free to subscribe your email for free email. See more articles below for further reading and understanding.

- How Much does Mortgage Loan Officer Earns as Salary or Commission?

- How to Become a Mortgage Loan Officer in Nigeria, Ghana, UK, Canada

- How To Get A Mortgage Loan: 7 Steps To Get Approved for first timers

- Perfection of Legal Mortgage in Nigeria Law and Procedure for Getting Loan Property

- Mortgage Loan Amortization Calculator – Schedule & Fixed Housing Interest Rates

- Top Mortgage Lenders for Low Interest Rate and No Down Payments for First Time Buyers

- How Much is Mortgage Payments? Calculate using Interest rate, Taxes and Insurance [Online Calculator]