What’s is 30-year fixed mortgage rates? This refers to the interest rates offered on home loans that have a fixed repayment period of 30 years. This means that the interest rate remains the same throughout the entire loan term, providing stability and predictability in monthly mortgage payments for borrowers.

Current Mortgage and Refinance Rates

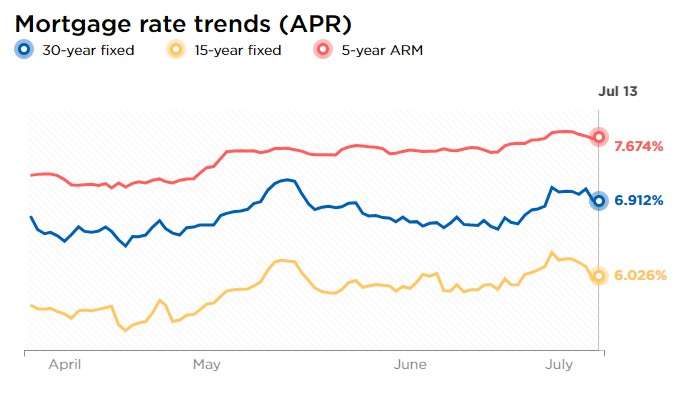

Accurate as of 07/13/2023.

| Product | Interest rate | APR |

|---|---|---|

| 30-year fixed-rate | 6.837% | 6.912% |

| 20-year fixed-rate | 6.705% | 6.814% |

| 15-year fixed-rate | 5.901% | 6.026% |

| 10-year fixed-rate | 5.861% | 6.055% |

| 7-year ARM | 7.118% | 7.654% |

| 5-year ARM | 6.893% | 7.674% |

| 3-year ARM | 6.125% | 7.204% |

| 30-year fixed-rate FHA | 5.617% | 6.523% |

| 30-year fixed-rate VA | 6.062% | 6.226% |

What is a 30-Year Mortgage?

A 30-year fixed-rate mortgage is the most common type of home loan that lasts for 30 years. It offers the advantage of having a stable payment amount for both the principal (the amount borrowed) and the interest. This allows borrowers to afford a larger loan amount since the monthly payments are lower compare to shorter-term mortgages for the same loan amount.

How do I Find Today’s 30-Year Mortgage Rates?

To find today’s 30-year fixed mortgage rates, you can use NerdWallet’s mortgage rate tool. It allows you to search for rates whether you’re purchasing a new home or refinancing your existing loan. Simply enter the necessary details about the loan you’re seeking in the provided filters, and you’ll receive a personalized rate quote instantly, without needing to share any personal information. This can help you initiate the approval process and make informed decisions regarding your mortgage.

What is a Good 30-Year Mortgage Rate?

Interest rates for 30-year mortgages can change frequently, even from hour to hour. To assess if today’s mortgage rates are favorable, it’s recommends to compare rates from multiple lenders. Obtaining rate quotes from different lenders on the same day allows for an accurate comparison.

It’s important to note that the loan offer with the lowest interest rate may not always be the best option. Lenders typically charge fees to cover their costs and generate profits. These closing costs can vary significantly among lenders, and the specific details may only be provided when you formally apply for the loan. Therefore, it’s important to consider both the interest rate and the associated closing costs when evaluating loan offers.

How do I Mortgage Rates Offers?

Determining whether a loan with higher interest rates and lower closing costs or a loan with lower interest rates and higher closing costs is better can be challenging unless you have expertise in financial matters. However, government regulations provide assistance by requiring lenders to furnish a Loan Estimate when you submit a complete loan application.

The Loan Estimate is a three-page document that outlines the loan’s specifics, estimated payments, and associated closing costs. On page 3 of the Loan Estimate, there is a section labeled “Comparisons.” This section allows you to compare the key details of different loan offers side by side, enabling you to make a more informed decision based on the provided information. It’s provides three subheadings:

- In 5 Years” totals how much you would spend on the mortgage in its first five years, including closing costs, principal, interest and mortgage insurance. A lower number is better.

- Annual Percentage Rate (APR) is a way to express the interest rate that takes closing costs into account. A lower APR is better.

- Total Interest Percentage (TIP) measures the total interest you would pay as a percentage of the loan amount. A lower TIP is better.

According to a report by Freddie Mac, it was found that a typical borrower has the potential to save approximately $600 to $1,200 per year by obtaining mortgage rate quotes from four different lenders instead of applying with just a single lender.

Pros and Cons of a 30-Year Fixed Mortgage

The 30-year fixed mortgage is the most popular term of home loan. It meets the needs of many borrowers, but some people prefer shorter loan terms. Here are benefits and drawbacks of the 30-year fixed:

Pros

- The monthly payments on a 30-year fixed mortgage are typically lower compare to loans with shorter terms. This is because the payments are spread out over a longer period of 30 years, making them more affordable on a monthly basis.

- A 30-year fixed mortgage offers flexibility in terms of payment options. If you have the financial capacity, you can make additional payments towards the principal to pay off the loan more quickly.

- Predictability. Because it’s a fixed rate, the monthly principal and interest payments are the same over the life of the loan. Property taxes and insurance can change over time, though.

- Bigger loan. Because monthly payments on a 30-year loan are smaller than on a shorter-term loan (such as 20 or 15 years), you can borrow more.

Cons

- 30-year fixed mortgage rates tend to be higher compare to loans with shorter terms, like 15 years. This is because the lender is extending the loan for a longer duration, which involves more risk and ties up their money for a longer period.

- More interest overall. You pay more interest over the life of a 30-year mortgage because you make more payments.

- A potential risk associated with a 30-year loan is the temptation to borrow more than necessary. With the ability to borrow larger amounts, there is a possibility of taking out a loan that exceeds your actual needs. Additionally, while you may be able to afford the monthly payments, it’s important to consider your overall financial situation.

How are Mortgage Rates set?

Mortgage rates are influence by market dynamics. Factors such as negative economic indicators or global political concerns can cause mortgage rates to decrease, while positive news can drive rates higher.

Lenders determine your specific mortgage rate based on the level of risk associated with lending to you. Generally, higher credit scores and larger down payments result in lower mortgage rates.

What’s the Difference Between Interest Rate and APR?

The interest rate is the percentage charge by the lender for borrowing money, while the APR (annual percentage rate) considers additional factors such as fees and discount points.

The APR serves as a useful tool for comparing different loan offers, even if they have varying interest rates, fees, and discount points.

Read Post:

- Adjustable-Rate Mortgage Loan: What is an ARM and How It Works

- Freedom Mortgage Loan Application and it’s Pros & Cons 2023 Review

- List of Documents Required for Mortgage Application in Nigeria [Home]

- Home Loan: How to Apply Mortgage, it’s Benefits and Documents Required

- What is Credit Facility? How it Works for Personal & Business Mortgage

- What’s Interest-Only Mortgage: How It Works and it’s Pros and Cons?

– Objectives, Impacts, Criticisms and Opinions")