Nigeria’s taxation system is a strong pillar of its economic architecture, serving as the primary mechanism for government revenue generation to fund public services, infrastructure, and development projects. As Africa’s largest economy with a population exceeding 220 million, Nigeria grapples with a tax-to-GDP ratio of around 10-13%, significantly below the global average for emerging markets (around 20-25%). This low ratio underscores systemic inefficiencies, over-reliance on volatile oil revenues, and widespread evasion, prompting ongoing reforms to broaden the tax base, enhance compliance, and promote equity.

The system has evolved dramatically, especially under the Bola Ahmed Tinubu administration, which enacted four landmark Tax Reform Acts in 2025: the Nigeria Tax Act (NTA), Nigeria Tax Administration Act (NTAA), Nigeria Revenue Service (Establishment) Act (NRSA), and Joint Revenue Board (Establishment) Act (JRBA). Effective from January 1, 2026, these laws consolidate over 60 fragmented taxes into fewer than 10, introduce digital compliance, and exempt low-income earners and small businesses to foster growth. However, as of January 18, 2026, the reforms face intense backlash, with controversies over alleged discrepancies in gazetted versions, calls for suspension, and public protests highlighting distrust in governance.

For entrepreneurs, businessmen, and traders—key drivers of Nigeria’s informal economy, which constitutes over 80% of employment—these changes present both opportunities and challenges. This article provides an in-depth exploration of the tax system, essential knowledge for business operators, prevalent problems, backlash, recommendations, and strategies to mitigate double taxation. Drawing from historical context, current structures, and recent developments, it aims to equip stakeholders with actionable insights for compliance and advocacy in a dynamic fiscal landscape.

Historical Evolution of Nigeria’s Taxation System

Understanding Nigeria’s tax system requires tracing its roots to colonial times. British colonial rule (1861-1960) introduced extractive taxation primarily to finance administration, including customs duties, poll taxes, and hut taxes. The Native Revenue Ordinance of 1917 formalized direct taxes in Northern Nigeria, while Southern regions followed suit in the 1920s. These regressive measures disproportionately burdened the people whose income is below the poverty threshold, people with low-income. This sparks uprisings like the 1929 Aba Women’s Riot against tax impositions by warrant chiefs.

Post-independence in 1960, the federal structure divided tax powers: regions handled income taxes, while the federal government managed customs and excise. The 1966 military coup centralized authority, leading to key legislations such as the Companies Income Tax Act (CITA) 1979, Personal Income Tax Decree 1993, and Value Added Tax (VAT) Decree 1993, which replaced sales tax with a 5% VAT (increased to 7.5% in 2020). The Federal Inland Revenue Service (FIRS) was established in 1993 to administer federal taxes.

Democracy’s return in 1999 decentralized aspects, with states gaining control over Personal Income Tax (PIT) via the Personal Income Tax Act (PITA) 2011. However, fragmentation persisted, resulting in multiple taxation and low efficiency. Reforms under Presidents Goodluck Jonathan and Muhammadu Buhari included the Voluntary Assets and Income Declaration Scheme (VAIDS) 2017 and annual Finance Acts (2019-2021), which digitized processes, taxed digital services, and incentivized compliance.

By 2023, when Tinubu assumed office, fiscal pressures—high inflation (over 30%), ₦87 trillion debt, and debt service consuming 96% of revenues—necessitated bold action. The Presidential Fiscal Policy and Tax Reforms Committee (PFPTRC), chaired by Taiwo Oyedele, proposed harmonization to reduce oil dependency (non-oil taxes contribute ~40% of revenue). The 2025 Acts build on this, but as of January 2026, implementation faces hurdles, including National Assembly probes into alleged “smuggled” provisions in gazetted laws.

All this history shows taxation as inherently political, intertwined with federalism, regional equity, and governance trust. For business owners, it underscores the need for adaptability amid evolving policies.

Overview of the Current Taxation Structure

Nigeria’s tax system operates on a multi-tiered federal framework, with revenues allocated via the Federation Account Allocation Committee (FAAC). The newly rebranded Nigeria Revenue Service (NRS, formerly FIRS) oversees federal taxes, State Internal Revenue Services (SIRS) manage state-level ones, and local governments collect minor levies.

Key taxes include:

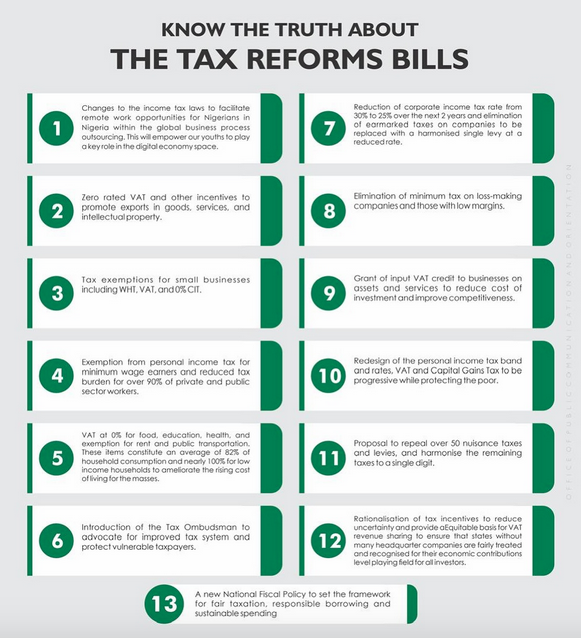

- Corporate Income Tax (CIT): Assessed on company profits. Large firms (>₦100 million turnover) pay 30% (phasing to 25% by April 2026 under NTA), medium (₦25-100 million) at 20%, and small (<₦25 million) at 0%. Petroleum firms face Petroleum Profits Tax (PPT) at 50-85%. Deductions cover capital allowances, R&D, and losses, but minimum tax is abolished.

- Personal Income Tax (PIT): Progressive, exempting incomes up to ₦800,000 annually. Rates: 15% (₦800,001-₦3 million), up to 25% (>₦50 million). Employees use Pay-As-You-Earn (PAYE); self-employed file self-assessments. Reforms replace relief allowances with capped deductions like rent relief.

- Value-Added Tax (VAT): 7.5% on goods/services, exempting basics (food, medicals, education, exports). Federally administered but shared: 15% federal, 50% states, 35% local (derivation-based), sparking Northern objections.

- Withholding Tax (WHT): 5-10% on dividends, interest, royalties, contracts; creditable against final liability.

- Capital Gains Tax (CGT): 10% on asset disposals, exempting personal residences (<₦150 million) and low-value gains. NTA aligns individual CGT with PIT rates.

- Stamp Duties and Other Levies: 0.5-2% on documents; new 4% Development Levy replaces sector levies (e.g., Education Tax). Digital assets now taxable.

The system is digitized via TaxPro-Max for filings, but informal dominance hinders reach. Tax treaties with 15 countries (e.g., UK, China) mitigate double taxation. In 2025, revenue hit ₦15.2 trillion, up 20%, but only 10 million active taxpayers exist.

What Entrepreneurs, Businessmen, and Traders Must Know

For business operators in Nigeria’s vibrant entrepreneurial landscape—from Lagos traders to Abuja tech startups—tax compliance is non-negotiable. Key obligations:

- Registration: All businesses must register with CAC and obtain a Tax Identification Number (TIN), now automatic via RC/BN numbers under NTAA. PoS operators face mandatory registration by January 2026 to combat fraud.

- Compliance Essentials: File annual returns by June 30 (companies) or March 31 (individuals). Use e-filing to avoid penalties (up to 25% fines, imprisonment). Track deductibles: rent, utilities, employee costs.

- Incentives for Businesses: NTA offers exemptions for small firms (<₦25 million turnover), R&D credits, and Economic Development Tax Incentives replacing Pioneer Status. Free zones provide tax holidays, but tightened (full tax on >25% domestic sales by 2028).

- Sector-Specific Notes: Traders in informal markets face presumptive taxation; crypto businesses must report digital assets. Importers/exporters navigate customs duties (0-35%) and VAT exemptions.

- Penalties and Audits: Non-compliance triggers audits, back taxes, and seizures. NRS’s AI tools enable real-time monitoring.

Entrepreneurs should engage tax consultants for planning, leveraging treaties for international trade. Recent Acts exempt 97% of SMEs from CIT, boosting confidence, but require digital literacy. There has been several meetings of Nigerian businessmen and entrepreneurs engaging in tax compliance activities in the past few months.

Problems Plaguing Nigeria’s Tax System

Despite reforms, systemic issues persist:

- Fragmentation and Multiple Taxation: Overlapping levies across tiers lead to harassment, discouraging investment. JRBA aims to harmonize, but implementation lags.

- Low Compliance and Evasion: Informal sector evasion costs billions; only 10% of potential taxpayers comply. Corruption scandals erode trust.

- Inequity and Regressivity: Poor bear disproportionate VAT burden; regional disparities favor oil states via derivation.

- Digital and Capacity Gaps: Low literacy hinders e-filing; NRS struggles with understaffing.

- Economic Volatility: Oil dependency exposes revenues to global shocks; debt service crowds out spending.

Recently, there has been controversies over law discrepancies amplify these, with experts noting 31 flaws in drafting.

Backlash and Controversies Surrounding the Tax Laws

The 2025 Acts have ignited fierce opposition. Public sentiment, per X discussions, leans toward rejection, viewing reforms as burdensome amid 25% inflation and poverty. Protests, led by youth and NANS, decry “taxing poverty,” predicting chaos like Kenya’s. Northern leaders oppose VAT derivation, fearing losses.

Allegations of “forgery”—discrepancies between passed and gazetted versions—prompted Assembly releases of CTCs, casting doubt on sanctity. Opposition figures like Peter Obi demand suspension, labeling laws “extortive.” A reported suspension of rollout adds uncertainty.

Tax experts from KPMG highlight inconsistencies, urging reviews. NRS defends, emphasizing no new burdens and benefits like tax cuts for 98% citizens. Backlash reflects “reform fatigue” from subsidy removal pains.

Recommendations for Enhancing the Tax System

To address issues:

- Strengthen Transparency: Publish clear guidelines, conduct public education via NRS portals.

- Boost Digital Infrastructure: Invest in training, subsidize tech for SMEs.

- Combat Evasion: Enhance AI audits, incentivize whistleblowers.

- Promote Equity: Review derivation formulas, expand progressivity.

- Stakeholder Engagement: Involve businesses in policy via JRBA.

- Monitor Implementation: Establish independent oversight for reforms.

Experts like Oyedele urge support, noting potential GDP boost to 4.4% in 2026.

Protecting Business Interests from Double Taxation

Double taxation—taxing the same income twice—poses risks for cross-border operations. Strategies:

- Leverage Tax Treaties: Nigeria’s 15 DTAs (e.g., with Netherlands) reduce withholding rates (5-10%). Claim credits via NRS forms.

- Structuring Entities: Use holding companies in treaty jurisdictions; avoid artificial arrangements to evade Permanent Establishment rules.

- Transfer Pricing Compliance: Document arm’s-length transactions per OECD guidelines; file declarations annually.

- Advance Rulings: Seek NRS pre-approvals for transactions.

- Group Relief: Consolidate losses within groups under NTA.

For traders, track foreign tax credits; consult professionals to optimize. Reforms introduce global minimum tax (15%) for MNEs, requiring vigilance. You can contact “The Nigeria Revenue Service” headquarters in Abuja, which is the central to tax administration for more updates.

Additional Considerations for Business Sustainability

Beyond basics, entrepreneurs should integrate tax planning into strategy:

- Crypto and Digital Assets: NTA taxes gains; report via self-assessments.

- Fuel and Gadget Impacts: Reforms affect prices via incentives/hidden taxes.

- SME Relief: 98% exemption threshold encourages formalization.

- Audit Preparedness: Maintain records for 7 years; respond promptly.

Amid controversies, businesses can lobby via associations for amendments.

Similar Taxation Updates

- The Role of The Attorney General in Taxation and Tax-Related Matters

- Tax implications on Cash-out Refinance for Homeowner rental property

- Legal Industry Adopts Cloud Computing for Solicitors & Law Firms

- Benefits of Registering your Business Name with CAC (Corporate Affairs Commission)

- Nigerian Tax Reform Bills (Acts) – Objectives, Impacts, Criticisms and Opinions

- Nigeria’s Tax System: Evolution, Reforms, Controversies, and the Tinubu Era

Statements from Notable people and Organizations about the Tax Reform Bill

Some notable people, experts, organizations, and bodies who have publicly spoken or released statements highlighting problems in Nigeria’s tax system (particularly the 2025 Tax Reform Acts effective January 1, 2026). These focus on issues like drafting errors, inconsistencies, gaps, policy contradictions, implementation risks, potential burdens on citizens/businesses, and constitutional concerns.

Peter Obi (Former Presidential Candidate, Labour Party)

He called for an immediate suspension of the new tax laws, citing 31 critical flaws including drafting errors, policy contradictions, administrative gaps, and complexities that could burden struggling citizens and businesses. He argued the issues are so severe that even experts needed private meetings to understand them, and warned against adding burdens amid economic hardship.

KPMG Nigeria (Global Accounting Firm)

In a detailed report titled “Nigeria’s New Tax Laws: Inherent Errors, Inconsistencies, Gaps and Omissions,” KPMG flagged multiple problems such as ambiguities in taxing non-residents, dividend treatment, foreign exchange deductions, capital gains computation (especially in high-inflation environments leading to taxing nominal rather than real gains), indirect share transfers, and withholding tax rules. They warned these could spark disputes, deter investment, cause over-taxation, and undermine reform goals, urging urgent amendments and guidance.

Manufacturers Association of Nigeria (MAN)

They described aspects of the reforms as a potential costly, bureaucratic nightmare that could erode gains from the Nigeria Tax Act 2025, highlighting erratic policymaking and skepticism among businesses and remote workers now in the tax net.

Northern Elders Forum

They criticized certain elements (e.g., related to digital aspects or revenue sharing) as “digital colonialism”, expressing concerns over unequal impacts and extraction favoring certain interests.

National Association of Nigerian Students (NANS)

They threatened nationwide protests over inadequate public enlightenment, alleged unauthorized alterations to the passed versions, and risks of increased distrust and hardship, demanding a suspension.

Oby Ezekwesili (Former Minister and Policy Expert)

She called for an immediate suspension due to constitutional and legal irregularities, alleging the gazetted version differs materially from the passed bill, undermining democracy, rule of law, and taxpayer protections, while raising federalism issues.

Cheta Nwanze (Analyst/Commentator)

In commentary, he noted the reforms are great in theory but face real-world skepticism, with erratic policymaking creating distrust and potential burdens on citizens already struggling.

Various Civil Society and Lawmakers (e.g., Rep. Abdussamad Dasuki)

They raised alarms over alleged tampering with the gazetted versions (differences from the National Assembly-passed bill), calling for transparency and investigations.

These statements reflect widespread concerns about trust, clarity, equity, and implementation in the tax reforms, amid the government’s defense that most issues are misunderstandings or deliberate policy choices.

Conclusion

Nigeria’s taxation system, reformed in 2025, holds promise for a tax-driven economy but faces implementation teething pains. For entrepreneurs and traders, knowledge of obligations, incentives, and protections is vital to thrive. While problems like evasion and backlash persist, recommendations for transparency and equity can pave the way forward. As Tegbe notes, these Acts aim to strengthen the economy—success depends on collective buy-in.

– Objectives, Impacts, Criticisms and Opinions")